Is drawdown right for you?

Drawdown is the default answer for most modern UK retirees with a defined-contribution pot, but it is not the right answer for everyone. The four branches below cover the situations where the choice is reasonably clear - before you sign anything irreversible, book a free Pension Wise session.

- 1 I want guaranteed income for life→ Buy an annuity (or use part of pot). Drawdown gives no guarantees.

- 2 I want flexibility + inheritance→ Drawdown is the standard answer. Pot stays invested, passes to beneficiaries (subject to April 2027 IHT change).

- 3 I want a one-off lump sum→ UFPLS - but watch tax. 25% tax-free, 75% taxable on top of other income.

- 4 I'm still working full-time→ Wait if you can; taxable withdrawal triggers MPAA, capping future DC contributions at £10,000/year for life.

The four post-2015 options at a glance

The 2015 pension freedoms (introduced by the Taxation of Pensions Act 2014) gave anyone aged 55+ with a defined-contribution pension four ways to take it. You can mix them, you can do them in stages, and you can split a single pot across providers. The choice is yours and reversible only in one direction - you can stop drawdown and buy an annuity later, but you cannot unbuy an annuity.

| Option | What you get | Tax treatment | Best for | Risks |

|---|---|---|---|---|

| Flexi-access drawdown | Pot stays invested; ad-hoc or regular taxable withdrawals after PCLS | 25% tax-free upfront (PCLS); rest taxed as income at marginal rate when drawn | Flexible retirees with other secure income; people wanting to leave money to family | Investment risk, sequence-of-returns risk, longevity risk, MPAA once taxable income taken |

| Lifetime annuity | Swap pot for guaranteed weekly/monthly income for life (single or joint) | 25% PCLS tax-free; annuity income taxed as PAYE income | People needing certainty; those without other guaranteed income | Irreversible; usually no money to beneficiaries (unless joint/guarantee); inflation risk if level |

| UFPLS | Take chunks of the pot ad-hoc; each chunk is 25% tax-free, 75% taxable | 25% of each withdrawal tax-free; 75% taxed as income at marginal rate | People taking occasional one-off lump sums without crystallising the full pot | Triggers MPAA; emergency-tax hit on first withdrawal; pot still exposed to markets |

| Full encashment | Take the whole pot in one go | 25% tax-free; remaining 75% taxed as income - usually pushes you into higher/additional rate | Very small pots (≤£10k trivial commutation); rarely optimal otherwise | Big tax bill, lose pension tax wrapper, MPAA triggered, no future drawdown flexibility |

The two routes to your tax-free cash

The 25% tax-free element is the same in both routes - but how you access it differs, and it matters for tax, flexibility and the MPAA trigger. The two HMRC-recognised mechanisms are PCLS (Pension Commencement Lump Sum, used alongside drawdown) and UFPLS (Uncrystallised Funds Pension Lump Sum, a hybrid lump sum). They are defined in HMRC's Pensions Tax Manual at PTM063210 (PCLS) and PTM063300 (UFPLS).

Crystallise (some or all of) the pot. Take up to 25% of the crystallised amount as a tax-free lump sum upfront. The remaining 75% goes into a drawdown account, still invested. Future withdrawals from the drawdown account are 100% taxable as income.

Worked example. Crystallise £200,000. Take £50,000 PCLS tax-free. The £150,000 left sits in drawdown; if you withdraw £20,000 next year, all £20,000 is taxable.

Use when: you want a big tax-free lump sum upfront (clear mortgage, buffer ISA) and regular taxable income afterwards.

Take a lump sum directly out of the uncrystallised pot. 25% of each withdrawal is paid tax-free and 75% is taxable income - automatically. No separate drawdown account.

Worked example. Pot £200,000. Take £20,000 UFPLS. £5,000 is tax-free, £15,000 is taxable as income that tax year. The rest of the £180,000 stays invested in the original pension, untouched.

Use when: you want ad-hoc lump sums without committing to a drawdown set-up; or you want to spread your 25% tax-free over many years.

Both routes trigger the Money Purchase Annual Allowance the moment you take any taxable money. Taking just the PCLS without any drawdown income does not trigger the MPAA - a small but useful loophole if you only need the tax-free cash.

Drawdown vs UFPLS - same £20k withdrawal, side by side

The two routes are not always tax-equivalent in the year you withdraw. PCLS-and-drawdown gives you a big tax-free chunk upfront and then 100% taxable income; UFPLS gives a smaller tax-free slice but on every withdrawal. For the same gross withdrawal in a given year, which leaves you better off net? This calculator does the maths on 2026/27 UK income-tax rates.

25% of pot = £50,000 tax-free (PCLS route).

Annual taxable income you want from the pot (PCLS aside).

Default = full new State Pension (£12,548).

Calculator uses full UK band stack; this radio is informational.

Take £50,000 as a one-off PCLS, then £20,000 of taxable drawdown income this year.

- Taxable this year

- £20,000

- Income tax

- £3,996

- Net from £20,000

- £16,004

Take £20,000 as a single UFPLS payment. Split automatically: 25% tax-free, 75% taxable.

- Tax-free slice (25%)

- £5,000

- Taxable slice (75%)

- £15,000

- Income tax

- £2,996

- Net from £20,000

- £17,004

Net this year, the UFPLS route keeps you about £1,000 ahead on the £20,000 of in-year income - before counting the one-off PCLS lump sum of £50,000.

With other income at £12,548 and a £20,000 withdrawal, PCLS-and-drawdown stacks all £20,000 on top - so the tax bill is higher in that year. UFPLS only stacks 75% × £20,000 = £15,000. UFPLS usually wins in-year tax; PCLS wins if you want the £ 50,000 cash upfront.

Approximate, 2026/27 UK rates excluding Scotland. Personal allowance £12,570; basic 20% to £50,270; higher 40% to £125,140; additional 45% above. Does not model the personal-allowance taper above £100,000, the MPAA trigger, emergency-tax adjustments, or the lifetime £268,275 Lump Sum Allowance cap. Always check exact figures with a regulated adviser or MoneyHelper before withdrawing.

Three named scenarios

Situation: Made redundant from a marketing role. Needs to bridge income for 9-ish years until her State Pension at 67 (she reaches the 67 cohort under the current SPA timetable).

Helen has a £80,000 SIPP from a previous workplace pension. She has 6 months of redundancy in the bank, no mortgage, and very little chance of returning to her old salary at her age. She needs the pension to plug a multi-year income gap, not last 30 years.

- Step 1 - take the PCLS. Crystallise the full £80,000, take £20,000 tax-free. £10k into a Cash ISA as a buffer; £10k clears a small home renovation she needed anyway.

- Step 2 - drawdown the remainder. The £60,000 sits in a drawdown account invested in a balanced multi-asset fund. She draws £8,000 a year taxable income for the next 9 years (to age 66, leaving a small buffer).

- Tax this year. Helen has no other income - the £8,000 sits entirely inside her £12,570 personal allowance, so it is paid tax-free. She does, however, trigger the MPAA the moment she takes the first taxable payment - capping future DC contributions to £10,000/year if she returns to work.

- NI gap warning. Years out of work between 57 and 67 are years she is not building her State Pension record. She should check her forecast on gov.uk/check-state-pension and consider voluntary Class 3 NICs to plug any gaps before SPA.

At 67 Helen layers the full new State Pension (£12,548 in 2026/27 terms) on top of whatever is left in the drawdown pot. If the pot grew at 4% real net of fees during the bridge years, she may still have £20,000-£25,000 left to top up retirement spending.

Situation: Earns £45,000 a year as an IT contractor. Doesn't plan to retire until 67. Wants to take some pension cash now to fund a kitchen renovation and an annual holiday - without retiring.

Mark is a textbook case for UFPLS rather than drawdown. He doesn't want a big upfront lump sum and his pension is much bigger than he needs for the bridge. He just wants £10,000 a year of extra spending money for the next five years.

- UFPLS option. Mark takes a £10,000 UFPLS each year. Each one is auto-split: £2,500 tax-free, £7,500 taxable on top of his £45,000 salary. Tax on the £7,500 at basic rate = £1,500. He nets £8,500 from each £10k withdrawal. The £290,000 left stays invested and growing.

- The MPAA trap - and how Mark avoids it for now. The moment Mark takes any taxable money - UFPLS or drawdown - his DC contribution allowance drops from £60,000 to £10,000 a year for life. Mark is contributing £8,000/year via his SIPP, so £10,000 still covers it - but if his contractor income rises and he wants to make a £30,000 one-off pension contribution before retirement, he can't.

- Alternative - phased PCLS-only. If Mark genuinely just wants tax-free cash, he could crystallise £40,000 a year and take the £10,000 PCLS slice tax-free, leaving the £30,000 (75% taxable portion) invested in drawdown but undrawn. This does not trigger the MPAA. He still gets £10,000 tax-free, with no tax bill at all. The trade-off: he has used up his PCLS entitlement on those slices and can't take more tax-free cash on them later.

The phased PCLS-only route is the unsung trick of the 2015 freedoms: you can keep saving heavily into a DC pension and take tax-free lump sums, as long as you never take any taxable income.

Situation: Widowed; has the full new State Pension plus a small final-salary pension of £6,000/year. £500k in a SIPP from years of higher-rate contributions. Two adult children.

Sandra doesn't need the £500k for income - her State Pension plus the final-salary pension covers her essentials. The pension is, in practice, an inheritance vehicle for her children. Under current rules to April 2027 the pot passes to her nominees free of inheritance tax.

- Conservative 3% withdrawal. Sandra takes £15,000/year from drawdown - well below the 3.9% Morningstar UK safe-withdrawal figure for 2025. With State Pension plus final-salary plus drawdown she has £33,500/year gross, and pays roughly £4,200 income tax, netting around £29,300.

- Pre-April-2027 IHT position. If Sandra dies tomorrow at 68, the remaining pot passes to her children tax-free (death pre-75 under current rules). If she dies at 76 the children pay income tax at their marginal rate on what they withdraw.

- Post-April-2027 IHT position. From 6 April 2027 the unspent pension joins her estate for IHT purposes. If her estate is over the combined nil-rate bands (~£500k-£1m depending on spouse residence nil-rate transfer), the pension above the threshold is taxed at 40% on death. Then the income-tax-on-death rules apply on top for post-75 deaths - a stacking the Treasury has been asked to soften.

- Planning response. Sandra should review her withdrawal strategy and consider gifting from income (which sits outside the 7-year IHT rule if it does not affect her standard of living). Increasing her drawdown income and gifting the excess can materially reduce the post-2027 IHT bill her children face.

Pension drawdown remains the most tax-efficient retirement vehicle for legacy - but the April 2027 change is the biggest single shift to UK retirement planning in a decade. Anyone using a DC pension as a primary inheritance vehicle should review their plan before the deadline.

The MPAA - don't accidentally trigger it

The first 5 years matter most

Tax on drawdown - the bit that catches people out

Emergency tax on the first withdrawal

April 2027 - drawdown pots into IHT

Free Pension Wise guidance - book before you commit

What UK retirees actually do

Beyond the marketing brochures, the FCA tracks what UK retirees genuinely do with their defined-contribution pots in its annual Retirement Income Market Data. The 2024/25 release covers the year to 31 March 2025 and is the most recent published at the time of writing.

"The total number of pension plans accessed for the first time in 2024/25 increased by 8.6% to 961,575 compared to 2023/24 (885,455). The overall value of money being withdrawn from pension pots increased to £70,876m in 2024/25 from £52,152m in 2023/24, an increase of 35.9%. Sales of annuities increased by 7.8% from 82,061 in 2023/24 to 88,430 in 2024/25. Enhanced annuity sales increased as a proportion of total guaranteed income for life sales, and now account for nearly half (48%) in 2024/25 compared to 38% six years ago."

Two takeaways. First, drawdown is the dominant regular-income route - flexi-access drawdown accounted for roughly a third of all plans accessed in 2024/25 (~350,000 of 961,575). Annuities accounted for about 9% (88,430). The remainder is mostly UFPLS and full-cash encashment of small pots. Second, annuity sales are growing again in absolute terms but drawdown is growing faster, and shop-around behaviour is at record levels: 62% of annuities are now bought away from the consumer's existing pension provider, the highest since the FCA began publishing the series.

A footnote - capped drawdown (pre-2015)

Before 6 April 2015, drawdown was tightly regulated under capped drawdown: an income ceiling set every three years using GAD (Government Actuary's Department) rates, designed to make the pot last roughly to age 99. Capped drawdown closed to new entrants on 6 April 2015 when flexi-access launched. Existing capped-drawdown plans can continue indefinitely - and a small minority of retirees prefer them, because staying within the cap means you do not trigger the MPAA and you can carry on making large DC contributions. The moment you exceed the cap, or convert to flexi-access, the MPAA fires.

SIPP drawdown vs personal pension drawdown

Mechanically, drawdown is the same product wherever you hold it. In practice the choice of provider affects fees, fund range and admin friction:

- Personal-pension drawdown (Aviva, Standard Life, Scottish Widows, PensionBee, Royal London): typically a single platform fee of 0.25-0.55% a year, a limited set of in-house multi-asset funds, and a streamlined drawdown set-up. Best for people who want simple and don't enjoy investment admin.

- SIPP drawdown (Hargreaves Lansdown, AJ Bell, Interactive Investor, Vanguard): a wider fund range (including individual shares, investment trusts and ETFs), often a tiered platform fee that caps in cash terms above £100k-£250k, and full control of withdrawal timing. Best for engaged investors with larger pots.

The drawdown rules are identical - both are flexi-access under the same HMRC regime - but on a £200k pot the difference in annual fees between a 0.45% all-in personal pension and a 0.25%-capped SIPP can be £400+ a year, compounding for 25 years. Run the numbers before consolidating, and watch for exit penalties on legacy with-profits or guaranteed-annuity-rate policies (those are usually worth keeping).

Frequently asked questions

Frequently asked questions

- What is pension drawdown?

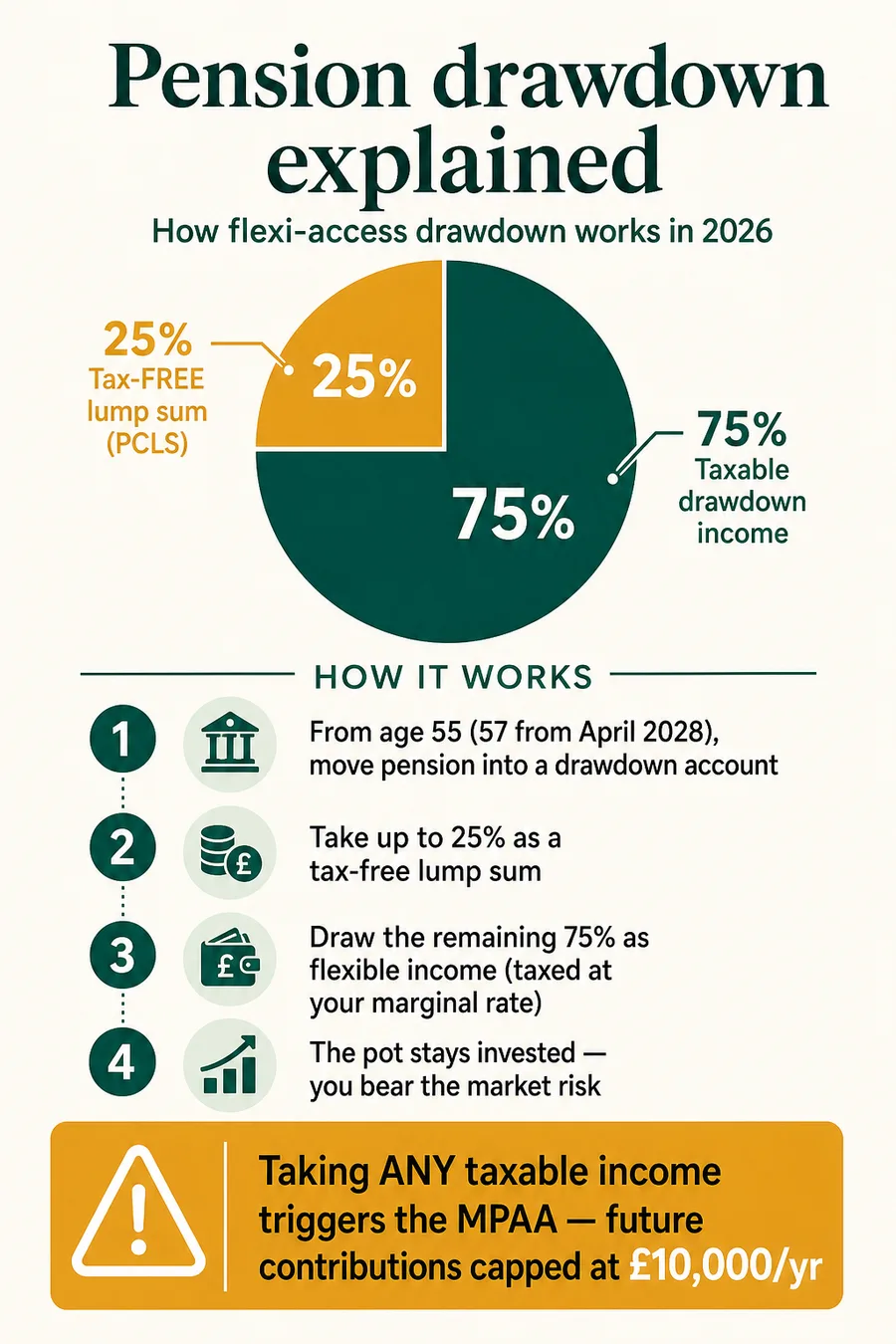

- Pension drawdown - formally "flexi-access drawdown" since the 2015 pension freedoms - is a way of taking income from a defined-contribution pension while keeping the rest of the pot invested. You can take up to 25% of the pot tax-free (the Pension Commencement Lump Sum, capped at £268,275 across all your pensions), and draw the remaining 75% as taxable income whenever and at whatever rate you like, from age 55 (57 from April 2028). The pot stays invested, so it can grow or shrink with markets - you take the investment risk, not an insurer.

- How does flexi-access drawdown work?

- You move some or all of your pension into a "drawdown account" with a SIPP or personal pension provider. At the point you "crystallise" funds you can take up to 25% as a tax-free lump sum (the PCLS), and the remaining 75% sits in drawdown invested in funds you choose. From there you take ad-hoc or regular taxable withdrawals via PAYE; you can change the amount, pause income, or stop entirely. You can also crystallise in chunks - taking a slice of tax-free cash and matching taxable income each year (phased drawdown). There is no upper income limit on the new rules.

- What's the difference between drawdown and UFPLS?

- Both are HMRC-approved ways of taking your DC pension. Drawdown (with a PCLS) separates your 25% tax-free cash from your taxable income: you take all or part of the 25% upfront and then draw taxable income from the crystallised pot. UFPLS - uncrystallised funds pension lump sum - blends the two: every withdrawal is 25% tax-free and 75% taxable, paid out of your uncrystallised pot. UFPLS is simpler for one-off withdrawals; PCLS-and-drawdown is more flexible if you want a big upfront tax-free sum and regular taxable income afterwards. Both trigger the Money Purchase Annual Allowance once you take taxable money.

- Can I take all my pension out at once?

- Yes - "full encashment" is one of the four post-2015 options. But unless your pot is small, taking it all in one tax year usually leaves you with a much larger tax bill than necessary. 25% is tax-free; the rest is added to your other income for the year and taxed at marginal rates. On a £200,000 pot, £150,000 of taxable income stacks on top of the State Pension and pushes most people deep into the 45% additional-rate band. HMRC almost always applies an emergency tax code to the first chunk, too, so you would then have to reclaim a refund via P53Z. Spreading withdrawals over several tax years almost always pays less tax.

- How is drawdown taxed?

- The 25% tax-free cash (PCLS) is paid free of UK income tax and does not use your personal allowance. Anything beyond that is taxable as income at your marginal rate in the year you take it, stacked on top of any State Pension, salary, rental or other income. The provider pays it through PAYE, almost always on a Month-1 emergency code for the first withdrawal - you usually need to reclaim via HMRC form P55 (still saving) or P53Z (pot emptied). Scotland has different rate bands. The 25% cap applies up to the Lump Sum Allowance of £268,275 across all your pensions combined.

- What happens to my drawdown pension if I die?

- Under current rules to April 2027, if you die before age 75 your remaining drawdown pot passes to your nominated beneficiaries tax-free, whether they take it as a lump sum or as income. If you die at or after age 75, the beneficiary pays income tax at their marginal rate on what they withdraw. From 6 April 2027 the government plans to bring most unused pension funds into the deceased's estate for inheritance tax - pensions will still pass to beneficiaries, but IHT may apply at 40% above the nil-rate band before the income-tax rules kick in. For estates around or above the £325,000 nil-rate band, this is a material planning change.

- Can I switch from drawdown to an annuity later?

- Yes - and many people do. Drawdown is reversible (you can use what is left to buy an annuity any time), but an annuity is not (once bought you cannot unwind it). A common strategy is to use drawdown in your 60s and early 70s while you have the energy to manage it and the appetite for some investment risk, then annuitise some or all of the remaining pot in your late 70s or 80s - by which point annuity rates are much higher because of the shorter life expectancy. Annuity rates also rise with health conditions: enhanced annuity rates for smokers or qualifying medical conditions can be 13-20%+ higher than standard.

- Do I have to take my 25% tax-free in one go?

- No. You can take the PCLS in slices over multiple tax years. This is called phased drawdown or "UFPLS-style" if you use the UFPLS rules: each crystallisation pays out 25% tax-free and 75% taxable in proportion. The advantage is that money left uncrystallised continues to grow tax-free inside the pension wrapper and (under current rules to April 2027) is more IHT-friendly on death before 75. There is no rule that forces you to take all your tax-free cash at retirement - you can leave it untouched indefinitely.

- What is the Money Purchase Annual Allowance?

- The MPAA caps how much you can pay into defined-contribution pensions and still get tax relief, once you have "flexibly accessed" your pension. From 2023/24 onwards the MPAA is £10,000 a year (down from the standard £60,000 Annual Allowance). It is triggered the first time you take any taxable income from drawdown, take a UFPLS payment, or buy certain flexible annuities - but NOT by taking just the 25% PCLS. Once triggered it applies for life: there is no way to undo it. If you are still working and saving heavily, this is the single biggest trap of starting drawdown too early.

- Is there a minimum amount I have to drawdown?

- No. Under flexi-access drawdown there is no minimum withdrawal - you can crystallise a pot, take the 25% tax-free cash (or part of it), and leave the rest invested without taking any taxable income at all. Providers usually have admin minimums for each payment (typically £100-£500), but no HMRC minimum. The old "capped drawdown" regime (closed to new entries from 6 April 2015) had a GAD-rate income ceiling but no floor either. If you already have capped drawdown you can stay on it indefinitely or convert to flexi-access - converting triggers the MPAA.