The two parts of every drawdown withdrawal

Every taxable pound that comes out of a defined-contribution pension is split into two halves. Understanding the split is the first step to understanding the tax, because the two halves are treated completely differently and travel along different routes from your pot to your bank account.

The 25% tax-free element - the pension commencement lump sum (PCLS), or the tax-free slice of a UFPLS - is paid free of UK income tax, does not appear on your tax code, does not eat into your personal allowance and does not count towards the personal-allowance taper at £100,000. You can take the full 25% in one go at the start, in slices each year (phased UFPLS), or alongside a regular drawdown income. The lifetime ceiling on the tax-free element across all your pensions is the £268,275 Lump Sum Allowance, in force since 6 April 2024 when it replaced the Lifetime Allowance. Most retirees never come close to it.

The 75% taxable element is pension income for tax purposes. HMRC's Pensions Tax Manual at PTM062730 puts it bluntly: "flexi-access drawdown pension is a form of pension for tax purposes and is chargeable to income tax as pension income". It is added to your State Pension, any earnings, any other pension income, rental profits and savings interest above the personal savings allowance, and the total is then taxed slab-by-slab through the bands set out below. Your pension provider deducts the tax under PAYE before the money lands in your bank account - the same machinery that taxes your salary, applied to your pension.

There is one important wrinkle. If you take a withdrawal as UFPLS (uncrystallised funds pension lump sum), every pound is split 25% / 75% as above. If you instead take it as flexi-access drawdown, you first crystallise a chunk of the pot, take all the tax-free cash from that chunk in one go, and then make taxable drawdown payments from the remaining 75%. Tax-wise the outcome over a full pot is identical; the difference is timing and provider mechanics. Most modern SIPP and workplace platforms support both; older contracts may force one or the other.

How much will you pay? A 30-second decision tree

Drawdown is taxed against your total income for the year - not in isolation. The four branches below cover the brackets you will sit in, based on the sum of your State Pension, any earnings, rental income, savings interest and the 75% taxable portion of every pension withdrawal. Add it all up before you decide how much to draw.

- 1 Total income under £12,570 (personal allowance)→ Pay nothing. Every pound up to £12,570 is covered by the personal allowance. Take whatever you need to fill the allowance - it is a use-it-or-lose-it slot.

- 2 Total income £12,570 - £50,270→ 20% on the bit above the personal allowance. Most pensioners with the full State Pension and a modest drawdown sit here. Basic-rate tax on roughly £15,000 of drawdown costs about £3,000.

- 3 Total income £50,270 - £125,140→ 20% on the first slice, 40% on the higher bit. Often caused by drawing a big one-off UFPLS, or still working while taking drawdown. Splitting across two tax years usually fixes it.

- 4 Total income above £125,140→ Plus 45% on the top slice, and your personal allowance has fully tapered to zero. The effective marginal rate between £100,000 and £125,140 is 60%. Avoid drawing here if you have any choice.

- 5 Scottish resident→ Different bands - six rates from 19% to 48%. See the Scottish section below for the exact thresholds.

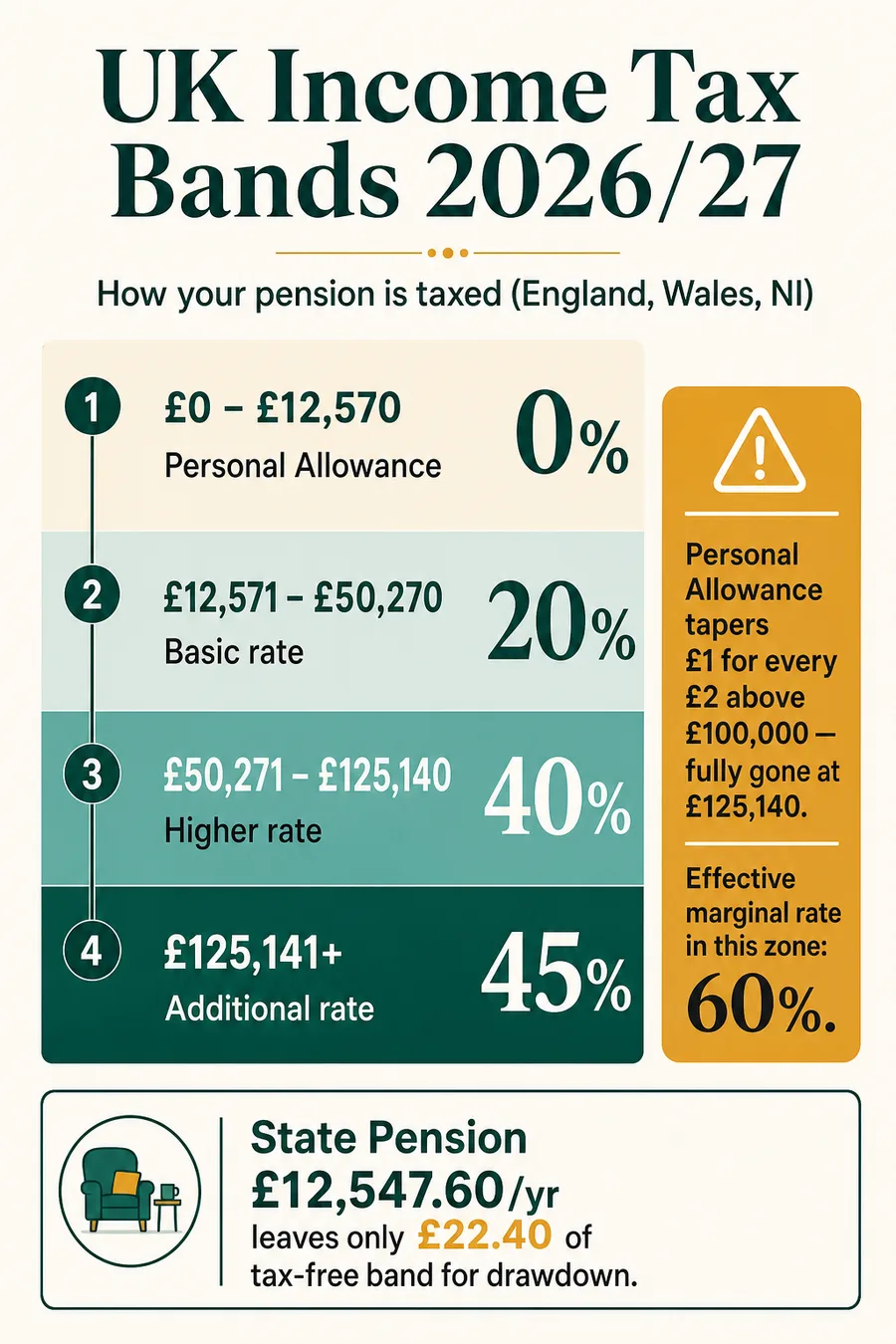

The 2026/27 income tax bands

Income tax in 2026/27 is charged in slabs. Each band only taxes the slice of income that falls within it - so a £30,000 income does not get taxed at 20% on the whole amount, only on the bit above the £12,570 personal allowance. Pension drawdown counts as non-savings, non-dividend income for tax purposes, which is the most heavily-taxed category. The same bands apply to earnings, the State Pension, occupational pensions and rental income.

| Band | Income range (E&W&NI) | Rate | Scottish equivalent |

|---|---|---|---|

| Personal allowance | £0 - £12,570 | 0% | 0% (same UK-wide) |

| Starter (Scotland only) | - | - | 19% on £12,571 - £16,537 |

| Basic rate | £12,571 - £50,270 | 20% | 20% on £16,538 - £29,526 |

| Intermediate (Scotland only) | - | - | 21% on £29,527 - £43,662 |

| Higher rate | £50,271 - £125,140 | 40% | 42% on £43,663 - £75,000 |

| Advanced (Scotland only) | - | - | 45% on £75,001 - £125,140 |

| Additional / top rate | Over £125,140 | 45% | 48% over £125,140 |

| Personal allowance taper | Above £100,000 of total income, £1 of personal allowance is lost for every £2 of income. Allowance is £0 at £125,140 - applies UK-wide. | ||

Personal allowance set by the UK Government and applies across the UK. Scottish bands set by the Scottish Parliament and apply to non-savings, non-dividend income (including pension drawdown) for Scottish-resident taxpayers. Confirmed by Scottish Budget 2026/27 and the rate-setting resolution passed in February 2026.

The State Pension trap - why everything else gets taxed

The full new State Pension is £241.30 a week, or £12,547.60 a year in 2026/27. The personal allowance is £12,570. That leaves precisely £22.40 of headroom before basic-rate tax bites. For anyone with a full or near-full State Pension entitlement, every pound of drawdown income - and every pound of taxable savings interest above the £1,000 personal savings allowance - is taxed at 20% from the first pound.

- Full new State Pension: £12,547.60

- UFPLS withdrawal: £20,000

- 25% tax-free element: £5,000 (does not use personal allowance)

- 75% taxable element: £15,000

- Total taxable income: £12,547.60 + £15,000 = £27,547.60

- Personal allowance: −£12,570 → taxable at 20%: £14,977.60

- Income tax: £2,995.52 - all at basic rate

- Net £20,000 withdrawal: £17,004.48

HMRC collects the tax owed on the State Pension by reducing your tax code on the drawdown provider's PAYE - the State Pension itself is paid gross.

If you have a partial State Pension because of missing National Insurance years, the maths is more forgiving - the unused part of your personal allowance shelters the first slice of drawdown. Conversely, if you have a final-salary pension on top, that pension stacks first, the State Pension on top of that, and drawdown on top of that. By the time drawdown is added, you may already be deep in basic-rate territory or even higher.

Two practical consequences. First, every pension provider operates its own PAYE feed with its own tax code; HMRC reallocates your personal allowance between them and applies a BR (20%) or D0 (40%) code to the others. Provider letters in March and April are worth reading because the coding is what decides what lands in your account. Second, the State Pension makes drawdown less tax-efficient than people expect - most of the "free" allowance gets used by it before drawdown gets a look in.

Your drawdown tax bill

Estimates UK income tax on a UFPLS-style drawdown (25% tax-free, 75% taxable) added to your other taxable income. Defaults to England/Wales/NI. Personal allowance taper above £100k applied automatically. Ignores National Insurance (none on pension income), savings interest beyond your other income, and dividends.

25% tax-free + 75% taxable.

State Pension + any wages, final-salary pension, rental. Default £12,547 = full new State Pension.

After tax your total annual income is £29,552 - that's £12,547 of other income plus the ££20,000 drawdown, minus ££2,995.4 of income tax for the year.

The taxable element of your drawdown is ££15,000. Your marginal rate on the next £1 of drawdown is the band you land in once everything is stacked. England, Wales and Northern Ireland rates apply.

Approximate. HMRC will probably apply an emergency Month-1 tax code to your first withdrawal - see the emergency tax section below for the P55 reclaim. Confirm any large withdrawal with your provider's PAYE projection or a regulated adviser before pressing the button.

Worked examples - £20,000 drawdown at three income levels

The same £20,000 UFPLS withdrawal generates wildly different net amounts depending on the income you already have. The table below shows three common cases for an England/Wales/NI-resident retiree taking a one-off £20,000 in 2026/27.

| Other income | Drawdown gross | Tax-free element | Taxable | Tax on this | Net drawdown received |

|---|---|---|---|---|---|

| State Pension only | £20,000 | £5,000 | £15,000 | £2,996 | £17,004 |

| State Pension + £20k other income | £20,000 | £5,000 | £15,000 | £3,000 | £17,000 |

| State Pension + £40k other income | £20,000 | £5,000 | £15,000 | £6,000 | £14,000 |

Calculated using 2026/27 bands: PA £12,570, basic to £50,270 (20%), higher to £125,140 (40%). "Other income" stacks first, drawdown 75% taxable element added on top. Tax on the drawdown is the difference between total tax with and without the drawdown - so the marginal-rate effect on the top slice is captured.

Three things to notice. First, the State-Pension-only case is the most efficient because the taxable drawdown sits entirely in basic-rate territory. Second, the middle row sees the same £20,000 gross drawdown deliver £3,000 less to your pocket than the first row because the slice above £50,270 catches 40%. Third, the worst case - when other income is already in higher-rate territory - turns a £20,000 gross withdrawal into about £14,000 net. The withdrawal does not change; the order of stacking does.

Three named scenarios

Situation: Just reached State Pension age. Wants a modest top-up to cover bills.

Pat takes the full new State Pension of £12,547.60 and a UFPLS withdrawal of £10,000 from her SIPP.

- State Pension: £12,547.60 (paid gross)

- Drawdown 25% tax-free: £2,500

- Drawdown 75% taxable: £7,500

- Total taxable income: £12,547.60 + £7,500 = £20,047.60

- Less personal allowance £12,570: £7,477.60 taxable at 20% = £1,495.52 income tax

- Net for the year: £12,547.60 + £10,000 − £1,495.52 = £21,052.08

Pat's effective tax rate on her £10,000 drawdown is just under 15% - better than the headline 20% basic rate because £2,500 of it was tax-free. PAYE collects the tax through her SIPP provider, and HMRC adjusts the tax code on the SIPP to account for the State Pension eating most of her allowance. No Self Assessment required.

Situation: Plans to wind down work over two years. Has been taking £8,000/yr drawdown to bridge a gap, but is now thinking about taking more.

Brian's salary is £45,000. He has not yet claimed his State Pension. He takes £8,000 of drawdown.

- Salary: £45,000 (already taxed at 20% above £12,570 - uses most of his basic-rate band)

- Drawdown 25% tax-free: £2,000

- Drawdown 75% taxable: £6,000

- Total taxable income: £45,000 + £6,000 = £51,000

- Stacking: the first £5,270 of taxable drawdown sits at 20% (filling the basic band to £50,270); the next £730 sits at 40%

- Tax on drawdown: £5,270 × 20% + £730 × 40% = £1,346

- Net £8,000: £6,654 - an effective rate of 16.8%

The smart play: defer drawdown until earnings stop. Once Brian retires next year and his salary drops to zero, the same £8,000 sits entirely in basic-rate territory (actually mostly inside his personal allowance if he times the tax year right), and the tax drops to roughly £400. Taking £8,000 of drawdown now to "make use of the pension" costs him ~£950 a year extra compared with waiting one tax year.

Situation: Comfortable retirement, takes a substantial annual UFPLS to top up holidays and home renovations.

Janet has the full new State Pension and an annual £30,000 UFPLS. Janet lives in Edinburgh, so Scottish rates apply.

- State Pension: £12,547.60

- Drawdown 25% tax-free: £7,500

- Drawdown 75% taxable: £22,500

- Total taxable income: £12,547.60 + £22,500 = £35,047.60

- Scottish bands applied: £0 to £12,570 at 0%; £12,571 to £16,537 at 19% = £753.54; £16,538 to £29,526 at 20% = £2,597.80; £29,527 to £35,047.60 at 21% = £1,159.39; total = £4,510.73

- Compare England/Wales/NI: the same £35,047.60 of taxable income would attract £4,495.52 - Janet pays about £15 more than an English equivalent at this income level.

At income above £43,662 the gap widens fast - Scottish higher rate is 42% versus 40% in England. If Janet were drawing £50,000 instead, the difference would be closer to £250-£300/year more in Scotland. Scottish rates apply because HMRC has Janet flagged as Scottish-resident based on her main home; the rates apply to all her non-savings, non-dividend income including her drawdown PAYE, regardless of where the SIPP provider is based.

The £100,000 cliff edge

Above £100,000 of total income, your £12,570 personal allowance tapers at the rate of £1 lost for every £2 over the threshold. By £125,140 the allowance is gone entirely. Inside that £25,140 band you pay 40% income tax on the slice plus a further 20% effective rate from the disappearing allowance - an effective marginal rate of 60%.

A higher-rate-paying drawdown taker who pushes total income from £100,000 to £101,000 pays £600 of tax on that £1,000. The smart move is to keep total income below £100,000 by splitting larger withdrawals across two tax years, paying voluntary pension contributions that the rules still allow you to make, or using ISA withdrawals to fund spending in years where you would otherwise hit the taper.

The Money Purchase Annual Allowance

Once you take any taxable income from a defined-contribution pension - even £1 of the 75% taxable element through UFPLS or flexi-access drawdown - you trigger the Money Purchase Annual Allowance (MPAA). From that day, your annual contribution allowance for DC pensions drops from £60,000 to £10,000 (the figure for 2026/27), and carry-forward of unused allowance no longer applies to DC pots.

Three things do not trigger the MPAA: taking the 25% tax-free PCLS on its own (without any taxable drawdown), buying a lifetime annuity, and small-pot lump sums of up to £10,000 from non-occupational DC schemes. Once triggered, the MPAA applies for every subsequent tax year - you cannot un-trigger it.

If you are still working and contributing meaningfully to a workplace pension, do not draw anything taxable until you stop accruing. See our guide to how drawdown works for the full rules.

Emergency tax on the first withdrawal

HMRC's PAYE systems treat the first taxable pension withdrawal as if it will repeat every month for the rest of the tax year. The provider applies a Month-1 emergency tax code - usually 1257L M1 - which projects your one-off £20,000 as if it were £240,000 over the year and taxes it accordingly. A £20,000 first UFPLS in spring can easily attract £4,500+ in tax instead of the £3,000 actually due.

Reclaim using P55 if you have not emptied the pot, P53Z if you have emptied the pot and have other taxable income, or P50Z if you have emptied the pot and have no other taxable income that year. HMRC repays within 30 working days. Full guide: emergency tax on pension withdrawals.

Marriage Allowance

If one spouse or civil partner earns below the £12,570 personal allowance and the other is a basic-rate taxpayer (income £12,571 to £50,270, or £43,662 in Scotland), the lower-earner can transfer £1,260 of personal allowance to the higher-earner. The recipient gets a tax reduction of £252 a year (£1,260 × 20%). It applies automatically once you elect, can be backdated four tax years (worth ~£1,000 in total), and carries on year after year until you cancel or your circumstances change.

Often relevant for retiring couples where one has a smaller pension. Apply through GOV.UK - see our Marriage Allowance guide for the eligibility detail.

Scottish residents - different bands

Scottish income tax has six bands in 2026/27. Pension drawdown is non-savings, non-dividend income, which means Scottish-resident taxpayers pay Scottish rates on it - not English rates - regardless of where their pension provider is registered.

- Starter rate 19% on income £12,571 - £16,537

- Basic rate 20% on income £16,538 - £29,526

- Intermediate rate 21% on income £29,527 - £43,662

- Higher rate 42% on income £43,663 - £75,000

- Advanced rate 45% on income £75,001 - £125,140

- Top rate 48% on income above £125,140 (introduced April 2024)

HMRC identifies you as a Scottish taxpayer based on where your main home is during the tax year - not where you were born or where you work. Move from Manchester to Glasgow midway through the year and your residence status (and which rates apply) is determined by where you spent the most days. Your tax code will be prefixed with an S (e.g. S1257L).

When drawdown forces Self Assessment

Pension drawdown is paid through PAYE, so the right tax is usually deducted at source. You are pulled into Self Assessment if:

- Total taxable income exceeds £150,000

- You owe tax that PAYE cannot collect (often the personal-allowance taper above £100k)

- You receive untaxed savings or rental income

- You take a deferred State Pension lump sum on the old (pre-2016) rules

- You want to claim higher-rate relief on personal pension contributions

- HMRC sends you a notice to file

Register through GOV.UK by 5 October following the tax year, file by 31 January, and keep the P60 your pension provider sends every May. Your provider's PAYE projection assumes you will draw at the same rate for the whole year - if your withdrawal pattern is lumpy, you may need to reclaim or top-up the difference at year end.

Seven legal ways to reduce drawdown tax

None of these is "tax avoidance" in the loaded sense - they are the way the rules are designed to work for a retiree who plans ahead. Use them in combination, and the same pension pot can deliver thousands more a year than a one-shot withdrawal would.

- Take only the 25% tax-free cash in years you need a lump sum. Most large one-off costs - clearing a mortgage, helping a child onto the housing ladder, a major car or home repair - can be funded entirely from the tax-free element if your pot is large enough. Leave the 75% inside the wrapper to grow tax-free and stay outside your taxable income.

- Spread larger withdrawals across two tax years. The single most powerful move. A £40,000 taxable withdrawal taken in March/April pays significantly less tax than the same withdrawal in a single year, because each half uses a fresh personal allowance and basic-rate band.

- Use ISA withdrawals to bridge. ISA money comes out tax-free and does not count towards your taxable income. In a year when you would otherwise tip into 40% tax or the £100,000 personal-allowance taper, fund the marginal spending from an ISA and leave the pension untouched.

- Fill the personal allowance every year. If your State Pension does not use the full £12,570 allowance, draw enough taxable drawdown to fill the gap each year. It is the only slice of withdrawal that is genuinely tax-free, and unused allowance cannot be carried forward.

- Time withdrawals around earnings. If you are still working and a higher-rate taxpayer on earnings alone, defer non-essential drawdown until earnings stop. The same withdrawal costs you 40% now and 20% later, with no other change.

- Use Marriage Allowance if you qualify. A lower-earning spouse can transfer £1,260 of personal allowance to a basic-rate-paying partner - £252/year, claimable for the four previous tax years (worth ~£1,000 in arrears). Often relevant when one partner has a much larger pension than the other.

- Mind the cliff edges. Three to watch. £50,270 (where higher rate starts). £100,000 (where the personal allowance starts tapering at an effective 60% marginal rate). £125,140 (where additional rate kicks in and the allowance is fully gone). A withdrawal that pushes total income £1 past any of these costs more than the same withdrawal £1 short.

If you have multiple pensions

Most people approaching retirement have at least two and often three or four pension pots - a current workplace scheme, one or two from earlier employers, sometimes a SIPP. Drawing taxable income from several at once is allowed, but creates a tax-coding puzzle. HMRC allocates your personal allowance to one pension (usually the largest by income, with tax code 1257L), and applies BR (20% flat) or D0 (40% flat) codes to the others. The total tax is right by the end of the year, but month-to-month it can look wrong, and over-deduction from one provider may need topping up by another.

Three practical tips. First, consolidate where it makes sense: bringing multiple small DC pots into a single SIPP simplifies tax administration enormously, and you can do this before crystallising any of them. Second, watch for the State Pension being coded out: because DWP cannot deduct tax at source, HMRC reduces the tax code of whichever pension is nominated to collect it. Read your March/April coding notices. Third, if you have an old final-salary scheme paying a fixed monthly amount, that is usually the simplest source to take the personal allowance against because the amount does not change year-to-year.

In HMRC's words - flexi-access drawdown taxation

HMRC's Pensions Tax Manual at PTM062730 puts it bluntly: "Flexi-access drawdown pension is a form of pension for tax purposes and is chargeable to income tax as pension income. The member receiving flexi-access drawdown pension is liable for income tax at their marginal rate in a tax year on whatever income they take from their flexi-access drawdown fund during that year. The scheme administrator is required to deduct income tax from the flexi-access drawdown pension under the PAYE regulations." The same rule applies whether you take income as regular flexi-access drawdown payments or as one-off UFPLS withdrawals - every taxable pound is taxed at your marginal rate.

Frequently asked questions

- How is pension drawdown taxed?

- The first 25% of each crystallisation is paid tax-free as a pension commencement lump sum, capped at the £268,275 Lump Sum Allowance. The remaining 75% is taxed as income in the year you take it, on top of your State Pension, any earnings, rental income or other taxable income. England, Wales and Northern Ireland use four bands in 2026/27 - 0% up to the £12,570 personal allowance, 20% to £50,270, 40% to £125,140 and 45% above. Scotland uses six bands, with a 19% starter rate, an intermediate 21% rate and a top rate of 48%. Your pension provider deducts the tax under PAYE before the money lands in your bank account.

- Do I pay tax on the 25% tax-free pension lump sum?

- No - the 25% pension commencement lump sum is paid free of UK income tax and does not eat into your personal allowance. Most people can take 25% of each pension up to a £268,275 ceiling called the Lump Sum Allowance, which replaced the Lifetime Allowance on 6 April 2024. The remaining 75% of the pot is taxable as income whenever you withdraw it. If you take the tax-free cash as a one-off lump sum at the start, that decision crystallises the pot - you cannot later take a fresh 25% from the same money.

- What tax do I pay on a £20,000 pension withdrawal?

- For a £20,000 UFPLS withdrawal in 2026/27, £5,000 (25%) is tax-free and £15,000 is taxable. If your only other income is the full new State Pension of £12,547.60, your total taxable income is £27,547.60 - the first £12,570 covered by the personal allowance, £14,977.60 taxed at 20%, so about £2,996 in income tax. Your net £20,000 withdrawal is therefore roughly £17,004. If you already earn enough to be a higher-rate taxpayer, the £15,000 taxable slice sits at 40% and the tax bill rises to £6,000. HMRC will probably apply an emergency tax code on the first payment - see our emergency tax guide for the P55 reclaim.

- Can I avoid tax on pension drawdown?

- You cannot avoid tax on the 75% taxable element entirely, but you can manage how much you pay. Keep total annual income below the £12,570 personal allowance and you owe nothing. Spread withdrawals across two tax years to stay inside the basic-rate band rather than tipping into 40%. Pair drawdown with ISA withdrawals, which are paid tax-free and do not count towards your taxable income. Take only the 25% tax-free cash in years you need a one-off lump sum. Avoid drawing right up to the £100,000 personal allowance taper or the £125,140 additional-rate threshold unless you have no choice.

- Is pension drawdown taxed in Scotland?

- Yes, and at Scottish rates if you are a Scottish-resident taxpayer. HMRC decides residence based on where your main home is during the tax year, not where the pension provider is. Scottish income tax has six bands in 2026/27: starter rate 19% to £16,537, basic 20% to £29,526, intermediate 21% to £43,662, higher 42% to £75,000, advanced 45% to £125,140 and a top rate of 48% above. Pension income falls under the Scottish rates for non-savings, non-dividend income. A Scottish-resident retiree drawing £30,000 of total income pays slightly more than an English equivalent because the intermediate rate kicks in at £29,527. The £12,570 personal allowance is the same UK-wide.

- How does the State Pension affect drawdown tax?

- The State Pension is taxable but paid gross - DWP does not deduct any tax before it reaches your bank account. In 2026/27 the full new State Pension is £12,547.60 a year, which uses up almost all of your £12,570 personal allowance and leaves only £22.40 of headroom. That means every pound of taxable drawdown you take on top is taxed at 20% from the very first pound. HMRC collects the tax owed on the State Pension by reducing the tax code that applies to your private pension PAYE stream. If your only income is the State Pension and you have no other income at all, you will pay no income tax - but the moment you add drawdown, the State Pension effectively becomes taxed by proxy.

- What is the personal allowance for pensioners?

- The personal allowance is £12,570 in 2026/27 - the same for pensioners as for anyone else. The old age-related allowances were abolished in 2016. The allowance has been frozen since 2021/22 and is currently scheduled to remain at £12,570 until at least April 2028 under the freeze announced in the 2022 Autumn Statement and extended by subsequent budgets. The allowance tapers above £100,000 - you lose £1 for every £2 of total income over £100,000, so at £125,140 the personal allowance is fully wiped out. Marriage Allowance lets a lower-earning spouse transfer £1,260 of personal allowance to a basic-rate-paying partner, saving the couple up to £252 a year.

- Why is my pension drawdown taxed at 40%?

- You hit 40% tax on the slice of total income above £50,270 in 2026/27. The State Pension, any earnings, rental and pension drawdown stack on top of each other. If you are still working on a £40,000 salary, taking £20,000 of taxable drawdown pushes your total taxable income to £60,000 and the top £9,730 sits at 40%. Big one-off UFPLS withdrawals are the most common cause: the £40,000 of taxable element from a £53,333 UFPLS, taken on top of a £12,547 State Pension, generates £52,547 of taxable income with £2,277 taxed at 40%. Splitting the same withdrawal across two tax years usually keeps every pound in the 20% band.

- Can I split drawdown withdrawals across tax years?

- Yes, and it is one of the most effective tax-management moves in retirement. The tax year runs 6 April to 5 April. If you need £40,000 from your pension and have only the State Pension as other income, taking it all in one year creates a bill of around £6,400; taking £20,000 before 5 April and £20,000 after creates a bill closer to £6,000 by keeping you below £50,270 each year. The maths becomes more powerful at higher income levels where one-off withdrawals would otherwise tip you into the 40% band or trigger the personal-allowance taper above £100,000. Some providers process flexi-access drawdown payments monthly or quarterly to even out the PAYE.

- Do I need to do Self Assessment for pension drawdown?

- Not automatically. PAYE deducts the right tax in most cases. You must register for Self Assessment if your total taxable income passes £150,000, if you owe tax that PAYE cannot collect, if you have untaxed savings or rental income over £10,000, if HMRC sends you a notice to file, or if you need to claim higher-rate relief on personal pension contributions. Drawdown above the £100,000 personal-allowance taper threshold is a common trigger. You also need to file if you receive a deferred State Pension lump sum on the old rules and HMRC has not coded it out. Register through GOV.UK by 5 October following the tax year and file by 31 January. Keep your provider P60s - drawdown is paid through PAYE and you get one each year.