Which is right for you? A 90-second decision tree

The right answer turns on four things only: how much guaranteed income you already have, how much you value flexibility, your health, and whether you want to leave money behind. Most full-length retirement guides spend pages dancing around this and never quite commit. The branches below are the answers regulated UK advisers actually give clients.

One framing that helps. Think of retirement income as two buckets: essential spending (housing, council tax, food, utilities, healthcare contributions) and discretionary spending (holidays, gifts, hobbies, cars). Essential spending should be matched to guaranteed income - State Pension, DB pension, an annuity. Discretionary spending can be funded by variable income - drawdown, dividends, ISA withdrawals. Decide your essential spending number first; then work backwards to how much guaranteed income you need to build, after the State Pension. That gap is your annuity allocation.

- 1 I worry about running out of money→ Buy an annuity - or at least annuitise a base layer big enough to cover essential bills alongside your State Pension. Longevity risk is what insurers exist to absorb.

- 2 I want to leave money to my family→ Drawdown - the remaining pot passes to nominated beneficiaries. Note: from 6 April 2027 unused DC pension funds fall into the IHT estate, so the legacy case is narrower than it was pre-Autumn 2024 Budget.

- 3 I want both guaranteed and flexible income→ Hybrid. Annuitise the floor (essential bills minus State Pension), drawdown the upside. This is what most advisers recommend for pots of £150k-£500k.

- 4 I have a health condition or smoke→ Get enhanced annuity quotes from at least three providers (Just, Canada Life, Aviva, L&G). Smokers, diabetics, heart and cancer patients typically see 15-25% higher rates - sometimes more.

- 5 I am under 65 and don't need the income yet→ Wait. Each year of age adds roughly 0.2 percentage points to a level annuity rate. Stay invested via flexi-access drawdown (or simply leave the pot uncrystallised) until you genuinely need the income.

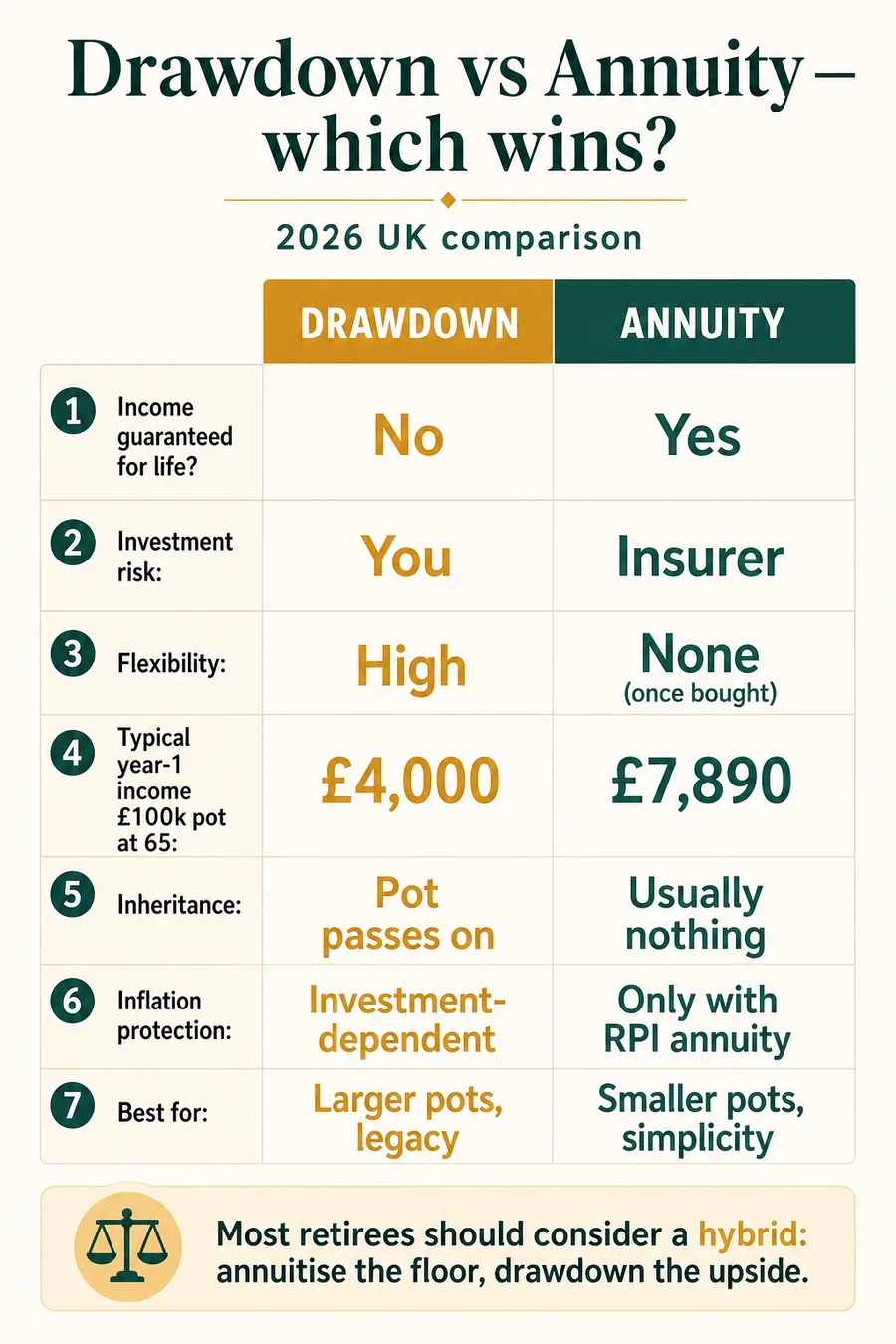

The head-to-head comparison

One table, two columns, the trade-offs that actually matter. Print this if it helps you commit.

| Feature | Drawdown | Annuity |

|---|---|---|

| Lifetime income guarantee | No - depends on returns and withdrawal rate | Yes - paid for life by the insurer |

| Investment risk | You bear it | Insurer bears it |

| Flexibility | High - vary income annually, take ad-hoc lumps | None - fixed at purchase, irreversible |

| Starting income from £100k at 65 | ~£3,900 (3.9% Morningstar 2025) | ~£7,892 (HL best buy, May 2026) |

| Tax on income | Marginal rate (20% / 40% / 45%) | Marginal rate (20% / 40% / 45%) |

| Death benefits | Passes to nominated beneficiaries; IHT applies on unspent DC funds from April 2027 (Autumn 2024 Budget). Income tax for beneficiaries depends on age at death. | Usually lost on death unless joint-life, guarantee period or value protection bought |

| Charges | Platform fee + fund fees (0.5-1.5% total) | Built into the rate - no ongoing charge |

| Inflation protection | Investment-dependent (real returns from equities) | Only if you buy an RPI or escalating annuity |

| Longevity protection | None - you bear the risk of outliving the pot | Full - paid until you die, even at 105 |

| Best for | Higher pots, secure base income elsewhere, legacy goals, comfort managing investments | Smaller pots, no other guaranteed income, dislike of risk, longevity in the family |

The simplest summary: drawdown is a flexible investment account that you happen to be drawing income from; an annuity is an insurance product that converts your pot into a paycheque for life. The first preserves optionality; the second insures against the worst outcome (running out of money in your 90s). Hybrid retirees buy a slice of both.

The single most under-rated row in the table above is "longevity protection". A 65-year-old man has a 1-in-4 chance of reaching age 92 according to ONS National Life Tables 2022-24; a 65-year-old woman has a 1-in-4 chance of reaching 95. Drawdown puts the entire risk of a long retirement on you. The annuity puts it on the insurer's balance sheet - the technical name is "mortality cross-subsidy", and it is the reason a healthy 65-year-old annuity rate of 7.9% exceeds any sustainable drawdown rate by such a wide margin. You are not getting a higher investment return; you are pooling longevity risk with thousands of other retirees, some of whom will die early.

Three routes with the same £200,000 pot

To make the trade-off concrete: imagine you are 65, have a £200,000 defined-contribution pot, and qualify for the full new State Pension (£12,547.60). Here is what each of the three main routes gives you in year one, before tax.

| Route | Year-1 income from pot | + State Pension | Capital remaining | Guaranteed? |

|---|---|---|---|---|

| 100% drawdown @ 3.9% | £7,800 | £20,348 | £200,000 invested | No |

| 100% level single-life annuity @ 7.89% | £15,780 | £28,328 | £0 (no inheritance) | Yes, for life |

| 50/50 hybrid (£100k annuity + £100k drawdown) | £11,790 | £24,338 | £100,000 invested | £7,890/yr guaranteed |

Worked example for illustration only. Assumes the full new State Pension £12,547.60 (2026/27), level single-life annuity at HL best-buy rate 7.89% May 2026, and Morningstar 3.9% sustainable drawdown rate. Before tax. The 25% tax-free cash sits outside this calculation - taking it does not change the income comparison structurally.

The 100% annuity route delivers nearly twice the income of 100% drawdown - but in exchange you give up the entire £200,000 of capital, all flexibility, and (unless you buy an inflation- linked or joint-life variant) any spousal cover. The 50/50 hybrid sits in the middle: about £4,000/year less than full annuitisation, but you keep £100,000 invested for emergencies, gifts, late-life care, or to pass on.

Break-even: when does the annuity beat keeping the capital?

The question every drawdown-curious retiree eventually asks: "At what age does the higher annuity income overtake the drawdown income, given I am also keeping the £200k pot intact?" The table below assumes the same £200,000 pot at 65: an annuity pays £15,780 a year forever; drawdown pays £7,800 a year with capital flat (no growth) or growing at 5% nominal.

| Year | Age | Cumulative annuity income | Cumulative drawdown income | Drawdown pot (flat) | Drawdown pot (5% growth) |

|---|---|---|---|---|---|

| 5 | 70 | £78,900 | £39,000 | £161,000 | £210,001 |

| 10 | 75 | £157,800 | £78,000 | £122,000 | £222,766 |

| 12 | 77 | £189,360 | £93,600 | £106,400 | £228,810 |

| 13 | 78 | £205,140 | £101,400 | £98,600 | £232,060 |

| 15 | 80 | £236,700 | £117,000 | £83,000 | £239,057 |

| 17 | 82 | £268,260 | £132,600 | £67,400 | £246,771 |

| 20 | 85 | £315,600 | £156,000 | £44,000 | £259,849 |

| 25 | 90 | £394,500 | £195,000 | £5,000 | £286,386 |

| 30 | 95 | £473,400 | £234,000 | £0 | £320,254 |

Cumulative income only - ignores tax (which is identical on both income streams at the same band) and inflation. Annuity rate 7.89% (HL best buy May 2026); drawdown rate 3.9% (Morningstar 2025). The "flat" pot column assumes no investment growth; the "5% growth" column assumes 5% nominal annual growth on the residual pot after each year's withdrawal.

Three readings of this table. First, on pure cumulative income the annuity overtakes drawdown at year 12-13 (highlighted) - by age 77-78. That is roughly average male life expectancy at 65 (18.7 years), and well below average female life expectancy (21.2 years). Second, factor in the residual capital: at year 13 the flat-pot drawdown route has £148,300 in cash plus the cumulative income, while the annuitant has nothing. Add them and drawdown is still ahead. Third, the 5% growth column: if your pot grows at 5% nominal, the drawdown pot actually rises during the early decades - you would be ahead on income plus capital indefinitely. Conversely, if returns are 2% or negative, the breakeven on income-plus-capital is closer to year 17-20.

Hybrid calculator - drawdown, annuity, or both

Use the calculator to model your own pot. We assume you take the 25% tax-free cash, then split the remaining 75% between an annuity and flexi-access drawdown. The annuity rate is picked from May 2026 best-buy figures for a healthy person at the age you choose.

25% tax-free: £50,000 · Working: £150,000

Annuity rate: 7.89%

Annuitised: £75,000

3.3% safer · 3.9% Morningstar · 4%+ riskier

Approximate, before tax. Annuity rates change daily with gilt yields; figures use HL/ Retirement Line May 2026 best-buy quotes. Drawdown sustainability depends on returns, inflation and sequence-of-returns risk. Get personalised quotes and free Pension Wise guidance before deciding.

Three real-world scenarios

Same maths, different lives. These three composite cases cover the most common decision points we see in the FCA's market data: DB-pension holder, single retiree on a DC-only pot, and a widowed retiree in poor health.

Situation: John has a £22,000/year DB pension from a long civil service career, plus the full new State Pension and a £150,000 SIPP from a private-sector second career. He owns his flat outright.

John already has the floor. His DB pension plus State Pension delivers £34,548 a year of guaranteed, mostly inflation-linked income - well above his essential spending and around the PLSA "comfortable" single standard. He does not need an annuity.

Right answer: full drawdown. He takes the £37,500 tax-free cash from the SIPP and reinvests it in his stocks-and-shares ISA. The remaining £112,500 stays in flexi-access drawdown, from which he plans to withdraw 4-5% (£4,500-£5,600/year) - used for travel, gifts to grandchildren, and the occasional big home repair.

Why not the annuity? Locking guaranteed income above what he needs would just lose the flexibility and the inheritability of the SIPP. From April 2027 the SIPP will fall into his IHT estate, but he plans to gift down over his lifetime - see our IHT on pensions guide.

Situation: Marie is single, healthy, just stopped work as an HR manager. £250k SIPP, mortgage paid off, no other guaranteed income except her State Pension. Wants security but also some flexibility.

Marie needs both halves. Without a DB pension, the State Pension alone (£12,547.60) sits below the PLSA "minimum" standard of £13,400. She has to build her own floor.

Right answer: hybrid. Take the £62,500 tax-free cash (some to a six-month emergency fund, the rest into ISA). Annuitise £100,000 of the remaining £187,500 at the level single-life rate of 7.89% - that buys £7,890 a year for life. Stack it with the State Pension and she has £20,438 of guaranteed income - covering all bills with a small surplus.

The other £87,500 in flexi-access drawdown. Marie withdraws 3.9% = £3,413/year for travel, family contributions and unexpected costs, with the pot still growing in real terms if markets average 5% nominal. Total Year-1 income: ~£23,850 before tax. Capital at risk: £87,500 - not zero, not all of it.

Situation: Trevor lost his wife in 2025. He has no other guaranteed income beyond the State Pension. Doctor estimates 10-15 year life expectancy given his cardiac history.

Trevor is the textbook enhanced-annuity case. A standard level single- life annuity at 70 might pay around 8.6%. With type 2 diabetes plus a documented heart condition, he should be quoted closer to 9.9% - possibly higher with the right underwriting. £250,000 × 9.9% ≈ £24,750/year for life.

Add the full new State Pension and he has £37,300 a year of guaranteed income, well above the PLSA "moderate" single standard of £31,700. Drawdown at 3.9% would only give him £9,750 from the £250k - leaving a £15,000-a-year gap he would have to fund from capital.

Why drawdown is the wrong call here. Drawdown rewards long retirements where compound growth on the residual pot outweighs the annuity income gap. Trevor probably will not live long enough to see that. Plus, drawdown requires ongoing investment management - exactly the cognitive task he should not have to do alone.

Shop three providers. Just Group, Canada Life and Aviva specialise in impaired-life pricing and quotes for the same medical history can vary by 15-20%.

Annuity rates in 2026 - why they actually look good

Annuity rates are a function of long-dated gilt yields. They collapsed from around 7% (2008) to barely 4% (2020) during the QE / zero-rate era - making annuitisation a hard sell. Since the Bank of England base rate began rising from 0.1% in late 2021 to over 5% by mid-2023, gilt yields have followed, and annuity rates have followed gilt yields.

May 2026 best-buy quotes from Hargreaves Lansdown show ~£7,892/year from £100,000 at age 65 (level, single-life, no guarantee). The William Burrows annuity index puts rates at their highest level for over a decade. ABI data confirms individual annuity premiums hit £7.4 billion in 2025 - the highest annual total since pension freedoms began in 2015, with annuities over £250k up 31% year-on-year. This is the best annuity market for new buyers in roughly 15 years.

One caveat: gilt yields drifted lower through early 2026 as inflation cooled. Rates may already be past peak. If you have decided on an annuity, there is a reasonable case against waiting another 12 months.

| Annuity shape | Age 60 | Age 65 | Age 70 | Age 75 |

|---|---|---|---|---|

| Level single-life | £7,120 (7.12%) | £7,890 (7.89%) | £8,620 (8.62%) | £9,650 (9.65%) |

| Level joint-life (50%) | £6,550 (6.55%) | £7,320 (7.32%) | £7,950 (7.95%) | £8,750 (8.75%) |

| RPI-linked single-life | £4,900 (4.90%) | £5,440 (5.44%) | £6,500 (6.50%) | £7,600 (7.60%) |

| Enhanced - smoker example | £7,900 (7.90%) | £9,070 (9.07%) | £9,900 (9.90%) | £10,850 (10.85%) |

Source: Hargreaves Lansdown Best Buy Annuity Rates (Aviva ~£7,892/£100k single-life level at 65, generated 7 May 2026), Retirement Line annuity rate tables (May 2026), Standard Life ("8.35% for a healthy 70-year-old", March 2026), Canada Life enhanced rates. Joint-life and older-age values triangulated from standard insurer pricing differentials. Always obtain a personalised quote - rates change daily with gilt yields.

Enhanced annuities - the most under-used uplift in UK retirement

Enhanced annuities - also called impaired-life annuities - pay a higher rate to people whose statistical life expectancy is shorter than average. Qualifying conditions include type 2 diabetes, high blood pressure, heart disease, stroke history, cancer (including in remission), COPD, kidney disease, obesity (BMI 35+) and regular smoking.

Typical uplifts are 15-25% for the most common conditions in retirees (diabetes, blood pressure, weight). Severe impairments can lift rates by 40-50%. June 2025 sample quotes for a 65-year-old "overweight smoker on medication for high blood pressure and high cholesterol" ranged from 6% (Legal & General) to 15% (Aviva) above standard.

Three rules. (1) Always shop at least three providers - rates for the same condition vary by 15-20%. (2) Be honest: misstating health invalidates the policy. (3) Use a specialist annuity broker (Retirement Line, HUB Financial Solutions, Better Retirement) - they have access to underwriters most direct-to-consumer sites do not. Specialist providers like Just Group and Canada Life dominate this niche.

The April 2027 IHT change - how it shifts the maths

In the Autumn 2024 Budget the Chancellor announced that from 6 April 2027 unused defined-contribution pension funds, and most lump-sum death benefits, will be brought into the deceased's estate for Inheritance Tax. The change applies to DC pensions, DB pensions and pensions already in drawdown. Exemptions remain for amounts passed to a surviving spouse, civil partner or registered charity.

What this changes for the drawdown-vs-annuity debate. Pre-2027, an unspent drawdown pot passed outside the estate - IHT free - making drawdown a genuinely powerful estate-planning tool. From April 2027, the inherited pot becomes IHT-assessable at 40% above the nil-rate band (£325k + £175k residence band where applicable). Income tax also applies if the holder died after 75.

The narrowed case for drawdown's legacy. If you are leaving the pot to a spouse, nothing changes. If you are leaving it to adult children, drawdown still has advantages over an annuity (capital remains, beneficiary can take income tax-efficiently over years) but the IHT-free wrapper is no longer one of them above the nil-rate band. See our full IHT on pensions explainer.

Pension Wise - the free 60 minutes you should book now

Before committing to drawdown, an annuity or a hybrid, every retiree aged 50+ is entitled to a free Pension Wise appointment via MoneyHelper. It is a one-hour conversation with a trained guidance specialist covering all four post-2015 options (annuity, drawdown, lump-sum withdrawals, leaving the pot invested) and the tax implications of each. It is not regulated advice - they will not tell you what to do - but it is the single best free starting point.

Book at moneyhelper.org.uk or by phone (0800 138 3944). Appointments are available by video or in-person at over 500 Citizens Advice locations. FCA data shows that retirees who use Pension Wise are more than twice as likely to shop around on annuity rates as those who do not.

The FCA's 2024/25 Retirement Income Market Data (published April 2025) puts the trend on record:

"Total number of pension plans accessed for the first time in 2024/25 increased by 8.6% to 961,575 compared to 2023/24 (885,455). Sales of drawdown policies saw the biggest increase from 278,977 in 2023/24 to 349,992 in 2024/25 (25.5%). Sales of annuities increased by 7.8% from 82,061 in 2023/24 to 88,430 in 2024/25. The overall value of money being withdrawn from pension pots increased to £70,876m in 2024/25 from £52,152m in 2023/24, an increase of 35.9%."

Drawdown still dominates by volume (roughly 4× annuity sales) but the gap is closing fast - annuity values keep setting post-2015 records (ABI: £7.4bn in 2025) as the post-2022 rate environment, larger pots and the April 2027 IHT change shift the balance.

Frequently asked questions

- Is an annuity better than drawdown?

- Neither is universally "better" - they answer different questions. An annuity is better if you want guaranteed lifetime income, hate market risk, or have a health condition that uplifts your rate. Drawdown is better if you want flexibility, expect to leave money to family, or have other guaranteed income (DB pension, rental) that already covers your essentials. At May 2026 rates a level single-life annuity at 65 pays ~7.89%/year for life, against a sustainable drawdown rate of ~3.9% (Morningstar 2025 research, 30-year horizon). The break-even on cumulative income is around year 12 - but drawdown leaves you with capital and inheritability that the annuity does not. FCA 2024/25 data shows drawdown sales outnumbered annuity sales roughly 4:1 (349,992 vs 88,430), though annuity volumes are growing fast (+24% in 2024 per ABI, hitting a ten-year high).

- Can I switch from drawdown to an annuity later?

- Yes - and this is a useful flexibility. You can stay in flexi-access drawdown for years, then use part or all of the remaining pot to buy an annuity. The annuity rate you receive will reflect your age at the point of purchase, so waiting from 65 to 70 typically uplifts your rate by 0.7-1 percentage point. Many advisers recommend annuitising gradually after age 70-75, when longevity risk rises and you may have less appetite for managing investments. The reverse - switching from an annuity to drawdown - is not generally possible once the annuity is in force.

- Are annuity rates good in 2026?

- Yes, by recent historical standards they are very strong. After collapsing from around 7% in 2008 to barely 4% in 2020 (the QE/zero-rate era), rates have recovered with the post-2022 rise in gilt yields. May 2026 best-buy quotes from Hargreaves Lansdown show roughly £7,892/year for life from £100,000 for a healthy 65-year-old (level, single-life). The ABI confirms 2025 individual annuity premiums hit £7.4 billion - the highest annual total since pension freedoms launched in 2015. That said, gilt yields softened through early 2026 and rates may be past their peak; if you are within a year or two of buying, the case for moving sooner rather than later is reasonable.

- Can I have drawdown and an annuity?

- Yes, and this hybrid approach is what most regulated advisers actually recommend for pot sizes between £150,000 and £500,000. You annuitise a slice - typically £75,000 to £150,000 - to create a guaranteed income "floor" that, with the State Pension, covers essential bills (housing, food, utilities, council tax). The rest stays in drawdown for travel, gifts, lumpy spending and to be passed to family. This protects you against running out of money AND against missing out on growth. You can also annuitise in stages: buy a small annuity at 65, another at 70, another at 75. This averages out the gilt-yield risk and lets each tranche benefit from age-related uplifts.

- What's the safest pension drawdown rate?

- Morningstar's 2025 retirement income research suggests 3.9% is the highest sustainable starting rate for a 30-year horizon at 90% probability of success, up slightly from 3.7% in 2024 and down from the original "4% rule" (Bengen, 1994). Morningstar separately points to 3.3% as a "very safe" rate that survives almost all historical scenarios including severe early-retirement bear markets. For UK retirees, the FCA's stochastic projection methodology supports a similar 3.5-4% band. Sequence-of-returns risk - a market crash in the first five years - matters more than the long-run average return, so a flexible rule (cut withdrawals after a bad year) typically does better than a fixed-percentage rule.

- Do annuities die with you?

- A single-life annuity with no guarantee period dies with you - that is why the income is highest. But you can buy: (a) a joint-life annuity, which continues paying 50% or 100% to your spouse or civil partner after you die (typically a 7-12% income hit on the starting rate); (b) a guarantee period of 5, 10 or even 30 years, which pays the income to your estate even if you die early; or (c) a value-protected annuity, which pays a lump-sum balance equal to what you paid in minus what you received. Each of these costs starting income. From April 2027, lump sums from annuities paid to anyone other than a spouse, civil partner or charity will fall into the IHT estate.

- Are drawdown and annuity income taxed the same?

- Yes. Both are taxed as earned income at your marginal rate (20% basic, 40% higher, 45% additional) once they exceed your personal allowance. The 25% tax-free lump sum (up to the £268,275 Lump Sum Allowance) is paid pre-tax in both cases. Where they differ is timing flexibility: drawdown lets you vary withdrawals year-by-year to stay below tax band thresholds, while an annuity pays a fixed taxable income that stacks on top of your State Pension whether you want it to or not. For a typical retiree with the full new State Pension (£12,547.60), the personal allowance is virtually used up, so almost every pound of annuity or drawdown income is taxable at 20% from pound one.

- Can I get a better annuity rate if I am ill?

- Yes - these are called enhanced or impaired-life annuities. Qualifying conditions include type 2 diabetes, high blood pressure, heart disease, stroke history, cancer, COPD, kidney disease, obesity (BMI 35+) and being a regular smoker. Uplifts range from around 6% (mild conditions) to 50% (serious impairments), with a typical 15-25% uplift for the conditions most common in retirees. Just Group, Canada Life, Aviva and Legal & General are the main providers. You must answer the medical questionnaire honestly - overstating conditions invalidates the policy, and understating them costs you income you were entitled to. Always shop three+ providers; rates for the same impairment can vary by 15-20%.

- Is drawdown risky?

- It carries three risks an annuity does not. (1) Investment risk: a 30%+ market fall in the first five years can permanently impair the pot - sequence-of-returns risk. (2) Longevity risk: if you live longer than expected and withdraw too much, the pot runs out. ONS National Life Tables 2022-24 put life expectancy at 65 at 21.2 years for women and 18.7 for men, with substantial tails - a 65-year-old woman has roughly a 1-in-4 chance of reaching 92. (3) Behavioural risk: drawdown requires you to keep making investment and withdrawal decisions in your 70s, 80s and 90s, often through cognitive decline. The annuity wins decisively on (1), (2) and (3); drawdown wins on flexibility, optionality and inheritance.

- Why are annuity sales up in 2026?

- Three reasons. First, rates: gilt yields rose sharply from 2022 onwards, taking annuity income back to levels last seen around 2010. ABI data shows individual annuity premiums hit £7.4 billion in 2025 - the highest since pension freedoms launched in 2015. Second, larger pots: ABI reports that annuities sold for pots over £250,000 rose 31% in 2025, and pots over £500,000 jumped 54% - the people who can afford to lock in a big guaranteed income are choosing to. Third, the April 2027 IHT change: drawdown's legacy advantage shrinks once unspent DC pots fall into the estate for inheritance tax, narrowing the case against annuitisation for retirees without spouses.