Which State Pension are you on?

There are two parallel systems. Which one applies to you depends entirely on the date you reach (or reached) State Pension age:

- 1 Yes→ You are on the old (basic) State Pension. Full rate 2026/27: £184.90 a week. You may also have Additional State Pension (SERPS / S2P) on top, plus any Graduated Retirement Benefit from before 1975.

- 2 No - and you have 35 qualifying years with no contracted-out service→ You get the full new State Pension: £241.30 a week.

- 3 No - 35 years, but with contracted-out years before 2016→ Your forecast may be lower than £241.30 because a Contracted-Out Pension Equivalent (COPE) was deducted in the 2016 starting-amount calculation. Keep working or paying NI and you can build it back up to £241.30, but not above.

- 4 No - fewer than 35 but at least 10 qualifying years→ You get a proportional amount (see the table below).

- 5 No - fewer than 10 qualifying years→ No new State Pension at all. Pension Credit may still be payable on a means-tested basis.

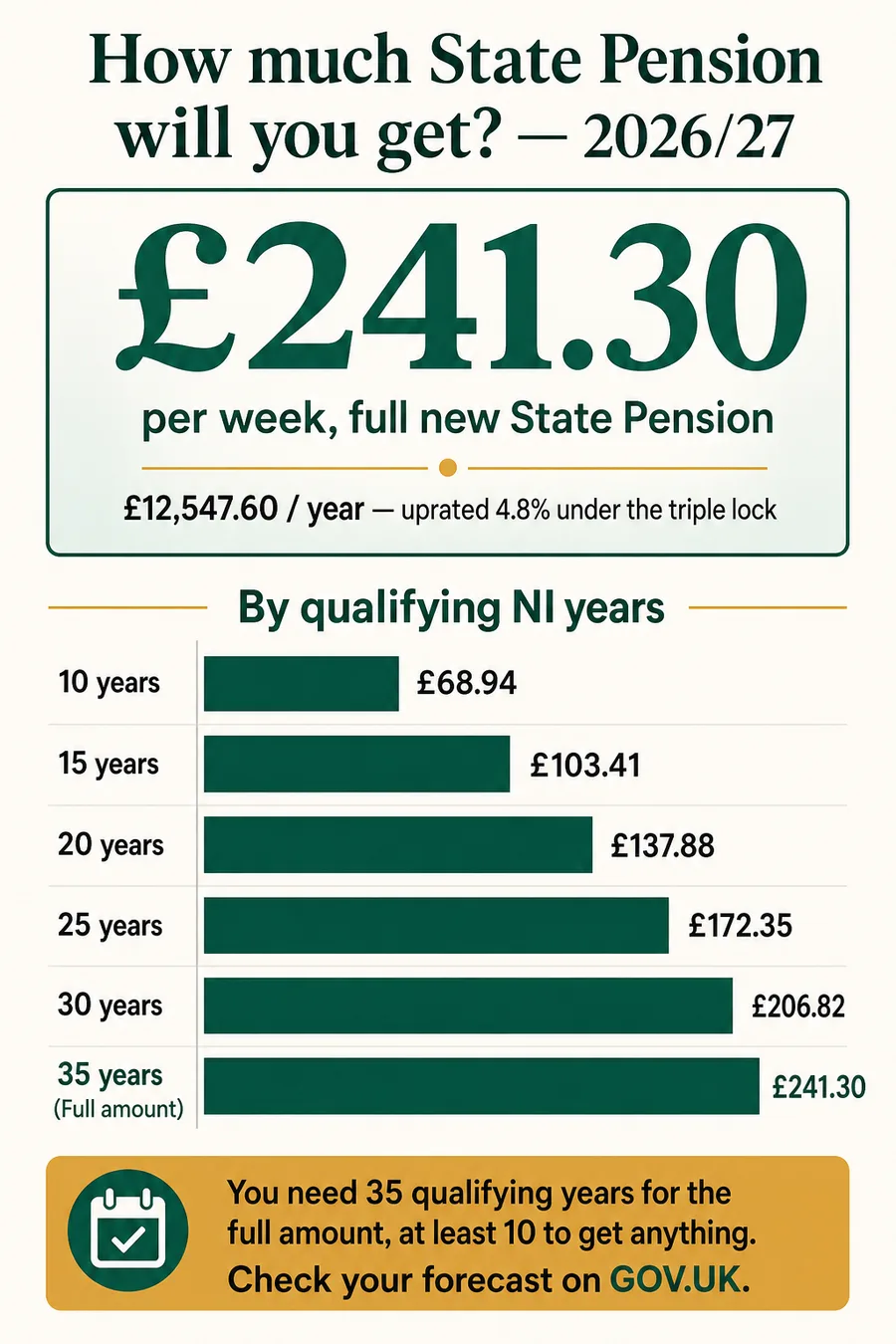

The 2026/27 rates - official figures

The Department for Work and Pensions confirmed the 2026/27 rates in late 2025, with the uprating taking effect on 6 April 2026. The House of Commons Library Benefits Uprating 2026/27 briefing walks through the numbers and the triple-lock arithmetic in more detail.

| Element | Weekly | Annual (52 weeks) |

|---|---|---|

| Full new State Pension | £241.30 | £12,547.60 |

| Full basic State Pension (Category A or B) | £184.90 | £9,614.80 |

| Category B lower (married woman's rate) | £110.80 | £5,761.60 |

| Maximum Additional State Pension (SERPS / S2P cap) | £230.54 | £11,988.08 |

How much you get by NI years - the full table

The new State Pension is broadly proportional to the number of qualifying years you hold, up to a cap of 35. Each qualifying year is worth 1/35th of the full rate - that's £6.89 a week, or about £358.50 a year, for every full year you build.

Calculated as years/35 × £241.30/week. Not exact for pre-2016 contracted-out years - see below.

| Qualifying NI years | Weekly | Annual | % of full rate |

|---|---|---|---|

| 10 | £68.94 | £3,585.03 | 29% |

| 15 | £103.41 | £5,377.54 | 43% |

| 20 | £137.89 | £7,170.06 | 57% |

| 25 | £172.36 | £8,962.57 | 71% |

| 30 | £206.83 | £10,755.09 | 86% |

| 34 | £234.41 | £12,189.10 | 97% |

| 35 | £241.30 | £12,547.60 | 100% |

| Fewer than 10 | £0.00 | £0.00 | 0% |

Your personal estimate

35 years or more - you are on track for the full £241.30 a week. Extra years above 35 don't add to your State Pension (though you keep paying NI if you're still working below State Pension age).

Rough estimate only. Pre-2016 service and contracted-out years can move your figure up or down - always confirm with your personal forecast on GOV.UK.

Three worked examples

Mark, 65, retiring in April 2027. Worked PAYE without any breaks from age 22 to 60, then drew NI credits while on Jobseeker's Allowance for two years. He has 41 qualifying years on his record - well above the 35 needed.

- Weekly State Pension: £241.30

- Annual: £12,547.60 (52 × £241.30)

- 4-weekly payment into his bank: £965.20

- With no other income, this is just £22.40 below the £12,570 personal allowance - so he pays £0 income tax on it. (If he later draws even £1 from a private pension, that £1 is fully taxable at his marginal rate.)

Sarah, 63, retiring in 2028. Worked from 18 to 25, took 10 years out of the labour market to raise children (Child Benefit credits for 8 of those years), and has worked full-time since. Her forecast shows 28 qualifying years.

- Pro-rata calculation: 28 ÷ 35 × £241.30 = £193.04 a week

- Annual: about £10,038

- 4-weekly payment: about £772

- She is 7 years short of the full rate. She has about 4 years until State Pension age and is working, so she will naturally add 4 more years (taking her to 32). To get all the way to 35 she would either need to keep working past State Pension age, defer, or buy 3 voluntary Class 3 years.

Dev, 66 in 2027. Worked 38 years in total, all PAYE, but for 16 of those years he was a member of a contracted-out final salary scheme - paying lower NI in exchange for building up a guaranteed minimum pension inside the workplace scheme.

- On a simple 38 ÷ 35 calculation he would expect the full £241.30.

- But his 2016 starting amount was reduced by a Contracted-Out Pension Equivalent (COPE) - DWP's estimate of what his contracted-out workplace pension makes up for. Suppose his 2016 starting amount was £140 (in today's money, after the COPE deduction).

- Every qualifying year he works after 6 April 2016 adds £241.30 ÷ 35 ≈ £6.89/week to that starting amount, up to the £241.30 cap. With 10 post-2016 years he'd be on roughly £140 + (10 × £6.89) = ~£209/week.

- The "missing" £32/week is compensated for by his contracted-out workplace pension - so his total pension is not actually lower. This is the single biggest source of "my forecast is less than I expected" surprises on GOV.UK.

Voluntary NI top-ups - is it worth it?

If your forecast shows a shortfall and you have gaps within the last 6 tax years, you can pay Class 3 voluntary contributions to plug them. The 2026/27 rate is £18.40 a week, or £956.80 for a full year. Self-employed people with profits under the small profits threshold can pay Class 2 voluntary contributions at the much cheaper rate of £3.65 a week (£189.80 a year).

The maths is unusually attractive - and the headline reason why this is one of the best-value financial decisions in UK personal finance:

- One year of Class 3 costs £956.80.

- Each extra qualifying year buys £6.89/week, or £358.50/year extra State Pension for life.

- Break-even: £956.80 ÷ £358.50 ≈ 2.7 years of receiving the pension. After that, you are in profit - and the State Pension itself rises with the triple lock.

- On average UK life expectancy at age 67, that's a 5-6× lifetime return on a single £956.80 payment.

The pre-2016 gap deadline - already passed

Between 2023 and April 2025 the government ran a one-off concession letting people fill NI gaps as far back as the 2006/07 tax year. That window closed on 5 April 2025 and has not been reopened. From 6 April 2025 the normal rule resumed: you can only pay voluntary contributions for the previous 6 tax years. At time of writing (May 2026) that means you can still fill gaps for roughly the 2019/20 tax year onwards. If you didn't fill earlier gaps before the April 2025 deadline, they are no longer recoverable under standard rules. See GOV.UK: voluntary NIC deadlines for the official position.

How to check your personal forecast

Don't rely on the table above for big decisions - get the official figure. The Check your State Pension forecast service is free, takes two minutes if you already have a Government Gateway login, and is the single most useful retirement-planning step most people can take.

- Go to gov.uk/check-state-pension and sign in with your Government Gateway ID (you'll need a passport, P60 or recent payslip to set one up).

- Look for three things on the forecast:

- "Forecast" - the figure you'll get if you keep contributing to State Pension age. This is the number that matters most.

- "Most you can get" - the cap. For most people this is the full £241.30/week in 2026/27 terms.

- Gaps and "you can fill" - years you can still top up, and the cost. Pay attention to whether topping up each year would actually move your forecast.

- If you contracted out at any point before April 2016, your COPE figure used to appear on the forecast - it's now reached by calling HMRC's NI helpline. Your forecast already has the COPE deduction built in.

Three real-world scenarios

James is 64, single, has worked continuously in PAYE roles since he was 18 - no career breaks, no contracting out. He will reach State Pension age at 66 (born before April 1960). On a back-of-envelope calculation he has 46 years of contributions, far above the 35 needed. His forecast will show the full £241.30 a week, or about £12,548 a year. With no other pension income beyond a small workplace defined-contribution pot, his State Pension alone falls just inside the £12,570 personal allowance - so it's tax-free at point of receipt. Action: nothing. He can ignore voluntary top-ups entirely. The only decision left is whether to claim at 66 or defer for a bigger weekly figure later.

Aisha is 60. She worked PAYE from 16 to 22, then again from 35 to 60 - a 13-year gap covering three children. She claimed Child Benefit for all three until each turned 12, so she has roughly 22 NI credit years stacked on top of 31 paid years - call it 28 qualifying years in total (some overlap with paid years). Her forecast shows £193.04/week (28/35 × £241.30), about £10,038 a year. She has 7 years to her State Pension age of 67. If she works full-time through them, she'll add 7 more years - taking her to 35 and the full £241.30. Action: she should check the Child Benefit credits actually transferred (the registration was optional pre-2010). She may have more years than she thinks. If a parent or grandparent cared for her children under 12 for some of those years, they could also claim Specified Adult Childcare Credits retrospectively.

Tony has been a self-employed plasterer since 1985. In leaner years his profits dipped below the small earnings exception and he didn't pay Class 2 - leaving 6 unfilled years on his record. His forecast shows 31 qualifying years and a figure of £213.72/week. To get to the full rate he needs 4 more qualifying years. Options: (a) keep trading and paying Class 2 for the 5 years until his State Pension age of 67 - covers it for around £18 a year each; (b) fill 4 of the recent gap years now with voluntary Class 2 at £3.65/week (£189.80/year) - a total cost of about £759 to buy £1,434.01 a year of extra State Pension for life. Break-even is around 14 months. The gap years from before 2019/20 are no longer fillable.

The triple lock and the 2026/27 uprating

The triple lock is the political commitment, in force since 2011, that the State Pension rises every April by whichever is highest of three measures:

- CPI inflation in the September before the new tax year;

- Average weekly earnings (AWE) growth, measured by the ONS over May-July of the previous year;

- 2.5% as a floor.

For 2026/27 the figures were:

- September 2025 CPI: 1.7%

- May-July 2025 AWE (total pay, including bonuses): 4.8%

- The 2.5% floor

Earnings won by a wide margin. The Secretary of State for Work and Pensions confirmed the 4.8% uplift in autumn 2025, taking the full new State Pension from £230.25 to £241.30 a week and the full basic State Pension from £176.45 to £184.90. Both rates apply from the first State Pension payday on or after 6 April 2026 - DWP and HMRC handle the change automatically; no claim is needed.

Political risk for future years. The triple lock is a manifesto pledge, not a permanent statutory mechanism. It has been suspended once (2022/23, when post-pandemic AWE distorted the comparison) and the cost - projected to push State Pension spending past 5% of GDP - is a recurring focus of Treasury reviews. Plan as if it stays in place, but don't assume the formula is untouchable across multi-decade horizons.

State Pension and tax

The State Pension is taxable income - but it is always paid gross, with no tax deducted at source. HMRC instead collects the tax through your other PAYE source: typically by reducing the tax code on a workplace pension, annuity or part-time job.

For 2026/27, the personal allowance is frozen at £12,570. The full new State Pension is £12,547.60. That leaves just £22.40 of headroom for anyone whose only income is the State Pension - and any other taxable income (workplace pension, savings interest above the personal savings allowance, rental income) sits fully on top, taxed at 20% from the very first pound. The government announced in late 2025 that pensioners whose only income is the basic or new State Pension would be spared a Simple Assessment for small tax amounts from 2027/28, but the detail of how this works is still being finalised.

For the full mechanics - including how your tax code is adjusted, what to do if you owe tax but are not in self-assessment, and the Marriage Allowance saving available to most pensioner couples - see State Pension and tax.

Frequently asked questions

Frequently asked questions

- Is the State Pension going up in 2026?

- Yes. From 6 April 2026 the full new State Pension rose by 4.8% to £241.30 a week (£12,547.60 a year), and the full basic State Pension rose to £184.90 a week (£9,614.80 a year). The 4.8% increase came from the triple lock - May to July 2025 average weekly earnings growth (4.8%) was higher than September 2025 CPI inflation (1.7%) and the 2.5% floor, so earnings set the uplift.

- How many years do I need for a full State Pension?

- For the full new State Pension (people reaching State Pension age on or after 6 April 2016) you usually need 35 qualifying years of National Insurance contributions or credits, and at least 10 years to get anything at all. The old basic State Pension required 30 qualifying years for the full rate. Qualifying years can come from paid Class 1, Class 2 or Class 3 contributions, or from NI credits - for example while claiming Child Benefit for a child under 12, while on Carer’s Credit, or while receiving Jobseeker’s Allowance.

- Do you get a State Pension if you have never worked?

- Possibly. Paid work is not the only way to build qualifying years. NI credits - for parents claiming Child Benefit for a child under 12, carers, people on certain benefits, or grandparents looking after a grandchild under 12 (Specified Adult Childcare Credits) - count toward State Pension. People who have built fewer than 10 qualifying years cannot claim any new State Pension. Pension Credit may still be available on a means-tested basis to bring income up to the minimum guarantee.

- What is the most State Pension I can get?

- On the new State Pension, the most you can earn through standard qualifying years is the full rate of £241.30 a week in 2026/27. But your figure can be higher if you have a "protected payment" from pre-2016 Additional State Pension (SERPS or S2P), or if you defer claiming and earn an uplift of 1% for every 9 weeks deferred (about 5.8% a year). On the old basic State Pension, Additional State Pension top-ups can take total weekly income well above £241.30; combined Additional State Pension is capped at £230.54 a week in 2026/27.

- Can I get the State Pension and a private pension?

- Yes. The State Pension is paid in addition to any workplace or personal pension you have. They are completely separate. You can take your private pension from age 55 (rising to 57 in April 2028) while the State Pension is paid from State Pension age - currently rising from 66 to 67 between April 2026 and April 2028. Both count as taxable income and are stacked together when working out the income tax you pay.

- How is the State Pension paid?

- The State Pension is paid directly into your nominated bank or building society account by BACS, every 4 weeks in arrears. It is not paid weekly or monthly by default. Your payday is set by the last two digits of your National Insurance number. The first payment usually comes a few weeks after you reach State Pension age and is back-dated to cover that period.

- When is the State Pension paid?

- It is paid every 4 weeks in arrears - covering the four weeks you have just lived through, not the four weeks ahead. The day of the week your payment lands depends on the last two digits of your NI number (00-19 Monday, 20-39 Tuesday, 40-59 Wednesday, 60-79 Thursday, 80-99 Friday). You can choose to be paid weekly instead if your weekly amount is below a low threshold, but most people are on the 4-weekly cycle.

- Does my partner’s State Pension affect mine?

- For people on the new State Pension (reached State Pension age on or after 6 April 2016) your entitlement is based on your own NI record only - your partner’s record does not boost it during their lifetime. On the old basic State Pension, married women and civil partners could claim up to 60% of their spouse’s basic rate if they had a poor record themselves. Inheritance rules still apply on death: a widow, widower or surviving civil partner may inherit part of a deceased partner’s Additional State Pension or protected payment, but not the standard new State Pension itself.

- Is the State Pension taxable?

- Yes - the State Pension is taxable income, but it is paid gross (with no tax taken off at source). HMRC collects any tax due by reducing the tax code on your other PAYE income such as a workplace pension or part-time job. In 2026/27 the full new State Pension is £12,547.60 a year and the personal allowance is frozen at £12,570 - leaving just £22.40 of headroom before any other income becomes taxable.

- Can I still fill old gaps in my National Insurance record?

- The special concession that allowed people to fill NI gaps as far back as the 2006/07 tax year ended on 5 April 2025. From 6 April 2025 onwards the normal rule applies: you can only pay voluntary contributions for the previous 6 tax years. As of May 2026, that means you can fill gaps from roughly 2019/20 onwards. Class 3 voluntary contributions cost £18.40 a week (£956.80 for a full year) in 2026/27. Always check your forecast on GOV.UK first - not every top-up actually increases your State Pension.