Which fits your situation?

Later-life lending is one of the few financial decisions that genuinely turns on a single question: can you reliably pay several hundred pounds a month, every month, for the rest of your life? If yes, RIO is almost always cheaper. If no, a lifetime mortgage is the product designed for your situation. Everything else is fine-tuning around that core question.

- 1 I have reliable pension income that comfortably covers a £400+ monthly mortgage payment - including after my partner dies→ A RIO mortgage is likely your cheapest option. Apply via a whole-of-market later-life broker - the affordability test is the real hurdle, not the rate.

- 2 I don't have enough pension income to pass a RIO affordability check, but I have meaningful equity in my home→ A lifetime mortgage is what this product was designed for. Use the Equity Release Council members list and insist on the no-negative-equity guarantee. Take the minimum lump sum you need and use a drawdown facility for the rest.

- 3 I'm comfortable now but worried about what happens if my partner dies first→ RIO lenders must stress-test single-life affordability. If you fail that test, look at a hybrid: a lifetime mortgage with voluntary partial repayments while you can afford them, falling back to roll-up if you can't.

- 4 I want to leave the maximum inheritance to my family→ RIO if you can afford it; otherwise a lifetime mortgage with the smallest possible drawdown and regular voluntary 10%-a-year repayments. The compounding maths is brutal - every year of payment-free interest doubles your future repayment burden.

- 5 I need a one-off lump sum for a specific purpose (care adaptations, helping family, debt clearance)→ Either can work. Compare the total 10-year cost on the exact amount you need - for sums under £30,000 the gap narrows. Don't forget downsizing as the third option.

Side-by-side comparison

The two products solve the same problem - releasing money from a home you own - but they sit in different parts of the FCA rulebook and behave very differently over time. The table below is the comparison most providers will not put in front of you on a single page.

| Feature | Lifetime mortgage | RIO mortgage |

|---|---|---|

| Monthly payments | None required (voluntary up to 10%/yr on ERC plans) | Mandatory interest payment every month |

| Affordability test | Minimal - based on age and property value | Full FCA affordability check, stress-tested for single-life |

| Rate type | Fixed for life (or capped, on a few plans) | Usually fixed 2-10 years, then reverts to lender SVR |

| Interest treatment | Rolls up and compounds monthly | Cleared each month - balance never grows |

| ERC consumer protections | Yes - five core ERC standards | No - not covered by ERC |

| Typical minimum age | 55 | 55, but most lenders set 60 or 65 |

| Eligibility | Age-driven LTV (~20% at 55 up to ~55%+ at 85) | Sufficient retirement income to service payments |

| What happens at death/care | Balance + rolled-up interest repaid from sale | Original balance repaid from sale |

| Inheritance impact (£80k borrowed, 20 yrs) | ~£297k owed against estate | £80k owed against estate |

| No-negative-equity guarantee | Yes (ERC standard) - estate never owes more than home sale price | Not applicable - debt does not compound past original balance |

| FCA regulation | MCOB equity release rules | MCOB residential mortgage rules (with retiree carve-out) |

| FSCS / FOS protection | Yes | Yes |

Rates and conditions reflect May 2026 market averages, drawn from the Equity Release Council Spring 2026 Market Report (lifetime mortgage band 6.40-7.20%) and the Moneyfacts retirement interest-only update (RIO band 6.30-6.80%). Individual lender terms vary - Aviva, Just, More2Life, LV=, Canada Life and Pure Retirement are the largest active lifetime mortgage lenders; Hodge, LiveMore, Leeds, Cambridge BS and a handful of regional building societies offer the most competitive RIO products.

Speak to an FCA-regulated equity release adviser

Compare lifetime mortgages and alternatives with a qualified later-life lending specialist. No fee unless you proceed.

Inline calculator: what would each cost you?

Default £80,000 - a typical UK release.

UK life expectancy at 70 is ~16 years (ONS 2022-24).

Used to compute the inheritance gap. Property growth ignored - both products are affected equally, so the relative gap is unchanged.

| Year | Lifetime mortgage balance | RIO balance | RIO paid so far |

|---|---|---|---|

| 5 | £111,107 | £80,000 | £25,218 |

| 10 | £154,311 | £80,000 | £50,437 |

| 15 | £214,313 | £80,000 | £75,655 |

| 20 | £297,647 | £80,000 | £100,873 |

After the home is sold for £350,000 (today's value, ignoring growth):

- Lifetime mortgage: estate receives roughly £52,353 after the £297,647 repayment.

- RIO: estate receives roughly £270,000 after the £80,000 repayment.

- Inheritance preserved by choosing RIO: £217,647.

Approximate. Lifetime mortgage interest assumes monthly compounding at the quoted annual rate (monthly equivalent rate). RIO interest assumes a constant rate for the term and ignores arrangement fees, valuation, advice fees and any product fees added to the loan. Get a personalised KFI from a regulated adviser before deciding.

Three real scenarios

Situation: Wants £80,000 to help her daughter buy a flat. Reliable indexed pension covers her bills with comfortable headroom.

Margaret's defined-benefit pension is the perfect RIO income - guaranteed, indexed, and not dependent on a spouse who could pre-decease. After essential costs she has more than £700 a month of free income.

- Product: RIO at 6.49% fixed for 5 years

- Monthly payment: £420 (interest only)

- Balance after 20 years: £80,000 (unchanged)

- Total interest paid: ~£104,000 over 20 years

- Estate at sale (assuming flat property value of £420k): £340,000 to her daughter

A lifetime mortgage in the same circumstances would leave only ~£123,000 of estate after 20 years - Margaret would have given her daughter the £80,000 now but cost her ~£217,000 of inheritance later. The arithmetic on a reliable pension comfortably favours RIO.

Situation: Wants £40,000 to clear small debts and replace a 12-year-old car. Cannot pass a RIO affordability test on State Pension alone.

Brian cannot service a RIO - no lender will pass an affordability check that leaves him under the personal allowance after the mortgage payment. A lifetime mortgage was designed for this situation.

- Product: Lifetime mortgage at 6.79% fixed for life (ERC member)

- Monthly payment: £0 required

- Balance after 15 years: ~£107,157

- Estate at sale (assuming flat property value of £300k): ~£192,843

Brian takes the £40,000 as a drawdown facility - releasing £15,000 now and reserving £25,000 for future need. Reserved funds do not accrue interest until drawn, which can save tens of thousands. He plans to make voluntary 10%-a-year repayments while he can, dramatically slowing the compounding.

Situation: Want £100,000 for home improvements and to gift to grandchildren. Susan's only pension dies with her - John worries she would fail single-life affordability.

This is the most common borderline case. They could pass a joint-life RIO affordability test today, but a stress test for John dying first leaves Susan with about £14,000 a year - and the lender would decline.

- Hybrid option: Lifetime mortgage at 6.79% with optional 10%-of-original voluntary repayments per year

- If both pay £541/month (the interest on £100k): the balance never grows - effectively a self-imposed RIO with no contractual obligation if Susan is widowed

- If voluntary payments stop after 8 years: balance picks up compounding from whatever level it was at - far less painful than 20 years of compound from day one

The Equity Release Council's March 2022 standards mandate the right to make penalty-free voluntary partial repayments on every new lifetime mortgage. Used assertively, this turns the product into a flexible RIO that drops its monthly demand the moment Susan needs it to.

When RIO wins

- You have a defined-benefit (final salary) pension, an annuity or a substantial drawdown income that comfortably covers the monthly payment after essential bills.

- Your income survives the death of one partner - DB pension with a 50%+ spouse benefit, two individual annuities, a healthy drawdown pot, or a survivor with their own State Pension and other income.

- Leaving an inheritance matters to you. RIO preserves typically £150,000-£250,000 more of estate than an equivalent lifetime mortgage held for 20 years.

- You only need the money for a fixed period (a five-to-ten-year bridge to selling and downsizing once a partner has died, for example). Over short horizons the gap between RIO and lifetime mortgage is much smaller.

- You want a rate that reverts to a market-priced SVR rather than being locked into today's rate for life. RIOs are usually fixed for 2-10 years then float; lifetime mortgages are fixed forever.

When a lifetime mortgage is the right answer

- Your income is too low or too variable to pass a RIO affordability check, including the stress test after first death.

- You expect to need the money for the rest of your life and you genuinely cannot guarantee to make a monthly payment every month for 20-25 years.

- You want absolute certainty that the lender cannot demand the money back or repossess for missed payments - ERC standards include the right to remain in your home for life.

- You want to fix today's interest rate forever rather than being exposed to RIO rate resets in 2031, 2036 and beyond.

- You want a drawdown facility - reserved funds that accrue no interest until drawn. RIO is usually a lump-sum product; lifetime mortgage drawdown facilities are common and save meaningful compounding on money you have not yet spent.

- You're in poor health and may qualify for an enhanced lifetime mortgage rate - a handful of lenders offer up to 5-15% more borrowing or a lower rate for qualifying conditions.

The RIO affordability test (and why it disqualifies so many people)

Under FCA mortgage conduct rules (MCOB 11.6), lenders must verify that a borrower can afford the monthly payment from sustainable retirement income - not just today but throughout the expected term. For RIO, that means the rest of your life. The FCA's 2024-25 mortgage market review identified two recurring failure points:

- Single-life income stress test. If you are a couple, the lender must model what happens when the first borrower dies. If the survivor's income (State Pension + any survivor benefit + any pension in their own right) does not cover the payment with margin, you fail.

- Variable drawdown income. Lenders heavily discount drawdown income because it is not guaranteed. A £20,000-a-year drawdown is often treated as £10,000 or less of "evidenceable" income.

This is the single biggest reason why lifetime mortgages outsell RIOs by roughly 10-to-1 in the UK. Many of the retirees who would benefit most from a RIO cannot pass the test - especially women, who tend to have smaller individual pensions and outlive male partners.

Regulation, protections and the no-negative-equity guarantee

Both lifetime mortgages and RIO mortgages are regulated by the Financial Conduct Authority under the Mortgages and Home Finance: Conduct of Business sourcebook (MCOB). Both require advice from an FCA-authorised adviser before sale, both are covered by the Financial Ombudsman Service for complaints, and both are protected by the Financial Services Compensation Scheme for adviser failure.

Lifetime mortgages additionally fall under the Equity Release Council standards, which are voluntary but adopted by the vast majority of UK lifetime mortgage lenders. The five core ERC standards are:

- A fixed or capped interest rate for the life of the loan, so the borrower can never face an unexpected rate shock.

- The right to remain in your home for life, or until the last surviving borrower moves into long-term care.

- The right to move to a suitable alternative property without penalty, subject to the new property meeting the lender's criteria.

- A no-negative-equity guarantee: when the home is eventually sold, the estate is never required to pay more than the sale price, no matter how much the rolled-up balance has grown.

- The right to make penalty-free voluntary partial repayments (mandatory on all new ERC plans since March 2022), typically up to 10% of the original loan per year.

RIO mortgages need none of these protections in the same way: the balance never grows, so there is no negative-equity risk; the rate is reviewed at remortgage anyway; and missed payments fall back on the lender's normal residential arrears process rather than triggering any equity-release-specific harm.

The FCA's supervisory guidance on later life lending (updated 2025) frames the duties plainly: "Later life lending products allow consumers to release equity from their homes to fund their retirement. These include lifetime mortgages, retirement interest-only mortgages and home reversion plans. Firms providing these products must act in the best interests of customers, ensure advice is suitable, and clearly explain the long-term costs and risks - including the cumulative effect of interest roll-up on lifetime mortgages and the affordability requirements for retirement interest-only mortgages."

Frequently asked questions

- What is the main difference between a lifetime mortgage and a RIO?

- Both are later-life mortgages secured on your home, and both are repaid only when you die, sell or move into long-term care. The big difference is what happens to the interest each month. With a retirement interest-only (RIO) mortgage you pay the interest as you go, so the balance you owe never grows. With a lifetime mortgage you pay nothing each month - the interest is added to the loan and compounds, so the balance can more than triple over 20 years. The other big difference is the affordability test: RIO requires you to prove your retirement income covers the monthly interest, whereas a lifetime mortgage has almost no affordability check at all.

- Is a RIO cheaper than a lifetime mortgage?

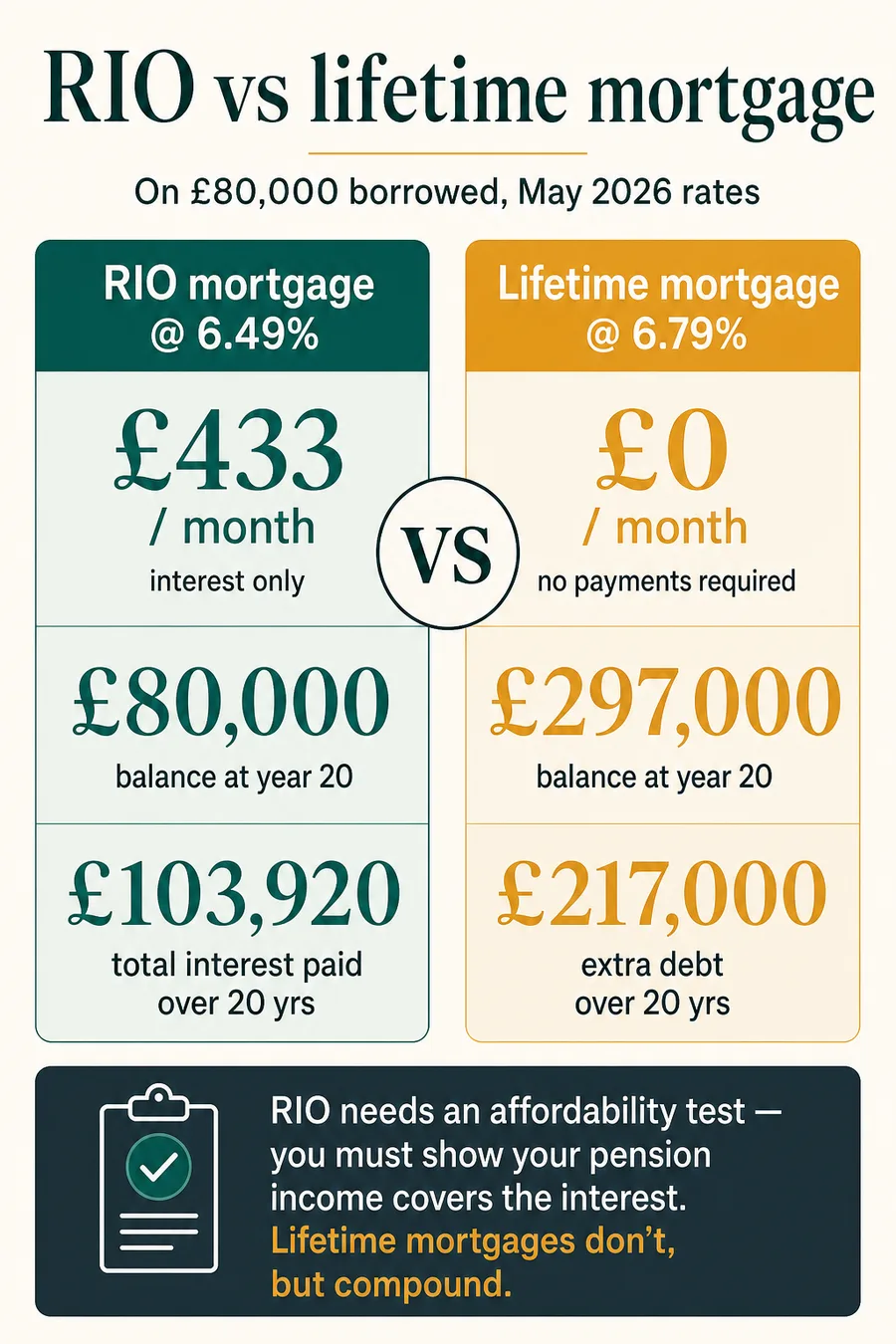

- Almost always, yes - sometimes dramatically. On a £80,000 loan at May 2026 indicative rates (6.49% RIO vs 6.79% lifetime), you would pay about £433 a month on the RIO and after 20 years still owe the original £80,000, having spent about £104,000 in interest. A lifetime mortgage at the same starting balance would owe roughly £297,000 after 20 years - about £217,000 in compounded interest. The catch is that "cheaper" only counts if you can actually afford the monthly RIO payment for the rest of your life.

- Why does a lifetime mortgage cost so much more over time?

- Compound interest. Because no payment is made, each month's interest is added to the balance, and next month's interest is then charged on the bigger balance. At 6.79% a year a debt roughly doubles every 10-11 years. On a 20-year horizon this is the difference between owing £80,000 (RIO) and owing nearly £300,000 (lifetime mortgage). The trade-off is that you keep all your income for living costs instead of handing several hundred pounds a month to the lender.

- Can I make voluntary payments on a lifetime mortgage?

- Yes, on most modern lifetime mortgage plans. Every Equity Release Council member plan since March 2022 must allow penalty-free partial repayments - typically up to 10% of the original loan per year. Used consistently, voluntary payments can keep a lifetime mortgage balance flat or even shrinking, blurring the line between a lifetime mortgage and a RIO. The benefit of doing it through a lifetime mortgage is that the payments stop being a contractual requirement the moment money is tight; on a RIO they are mandatory.

- What is the affordability test for a RIO mortgage?

- Under FCA mortgage rules, RIO lenders must check that your retirement income - typically State Pension, defined benefit pension, drawdown or annuity income - comfortably covers the monthly interest after essential costs. Crucially they must also stress-test what happens after the first death in a couple, because that often removes a significant slice of income. If you cannot evidence pension income that survives single-life, many lenders will decline you. There is no equivalent test for a lifetime mortgage, which is why lifetime mortgages exist as the safety net for older borrowers without the income to service a loan.

- Are both products regulated by the FCA?

- Yes. Both lifetime mortgages and RIO mortgages are regulated mortgage contracts under FCA rules - the Mortgages and Home Finance: Conduct of Business sourcebook (MCOB). RIOs sit in the standard residential mortgage rulebook with a carve-out from affordability rules for retirees; lifetime mortgages sit in the equity release rulebook. Both require advice from a regulated adviser before sale, and both are covered by the Financial Ombudsman Service and the Financial Services Compensation Scheme.

- Does the Equity Release Council cover RIO mortgages?

- No. The Equity Release Council standards apply only to lifetime mortgages and home reversion plans. The five core ERC guarantees - fixed or capped rate, no-negative-equity guarantee, right to remain in your home for life, right to move to a suitable alternative property, and the right to make penalty-free voluntary repayments - exist precisely because of the risks of rolled-up interest. RIO mortgages do not need a no-negative-equity guarantee because the balance never grows.

- What happens at death or going into care?

- Both products become repayable. With a RIO the lender is owed the original balance - usually settled from the proceeds of selling the home. With a lifetime mortgage the lender is owed the original balance plus all the rolled-up compound interest. On both, executors typically have around 12 months to sell the property; if the proceeds fall short on a lifetime mortgage, the Equity Release Council's no-negative-equity guarantee means the estate is not chased for the shortfall.

- Which product preserves more inheritance?

- RIO, almost without exception. Because you have been paying the interest as you go, the balance owed when the home is sold is the same as what you borrowed. A lifetime mortgage at 6.79% on £80,000 leaves about £297,000 owed after 20 years, eating a much larger chunk of any sale proceeds. On a £350,000 home that is the difference between leaving about £270,000 to family (RIO) and about £53,000 (lifetime mortgage). If inheritance matters to you and you have the income, RIO wins.

- Can I switch from a lifetime mortgage to a RIO later?

- In principle yes, by remortgaging - but it is rare in practice. Most retirees who started on a lifetime mortgage either could not pass a RIO affordability test in the first place, or saw their income fall after one partner died. By the time a switch is being considered, the rolled-up balance is also bigger than the original loan, making the new RIO repayment higher. Specialist later-life mortgage brokers are the right people to ask: the answer turns on your specific income, age, balance and property value.

Speak to an FCA-regulated equity release adviser

Compare lifetime mortgages and alternatives with a qualified later-life lending specialist. No fee unless you proceed.

- Free, no-pressure first chat, typically by phone or video

- Whole-of-market comparison across FCA-regulated lenders

- You stay in control and decide if you take it any further

RetirementExpert is an information service, not an adviser. By submitting this form you consent to being contacted by an FCA-regulated equity release specialist.