Is downsizing right for you?

Downsizing is usually framed as a money decision. It rarely is. The financial case is straightforward - release tax-free capital, cut running costs, sometimes secure a more manageable home for the next twenty years. The harder questions are about where you want to be, who you want near you, and whether you can face packing up forty years of life. Use the check below to work out whether to start ringing estate agents this week, or whether one of the alternatives (equity release, a retirement interest-only mortgage, or simply staying put with home improvements) is a better fit.

- 1 My home is far too big, the garden is a chore, and I want to release £150k+ of cash→ Downsizing is likely your best route - the maths comfortably beats equity release at this gap. Use the calculator below to confirm net release after stamp duty and fees.

- 2 I love my home and area, but I want to release some cash without moving→ Look at equity release or a RIO mortgage instead. Be very clear-eyed about the compound interest cost over 15-20 years - see the comparison further down.

- 3 I need to move closer to family or a hospital, even if the financial release is small→ Move anyway - the non-financial value usually dominates. Optimise within the constraint (target a town where prices give you some equity release as a bonus, not the primary goal).

- 4 I can't physically manage stairs / bathroom / garden anymore→ A single-storey home (bungalow, ground-floor flat, retirement village apartment) is often more valuable than the cash release. Prioritise accessibility features over postcode.

- 5 My partner has passed away, and the house feels too big and quiet→ Wait at least 12 months if you can - bereavement decisions about housing are statistically the most regretted. When you do move, prioritise community (proximity to family, walkable amenities, a retirement village if you want built-in neighbours).

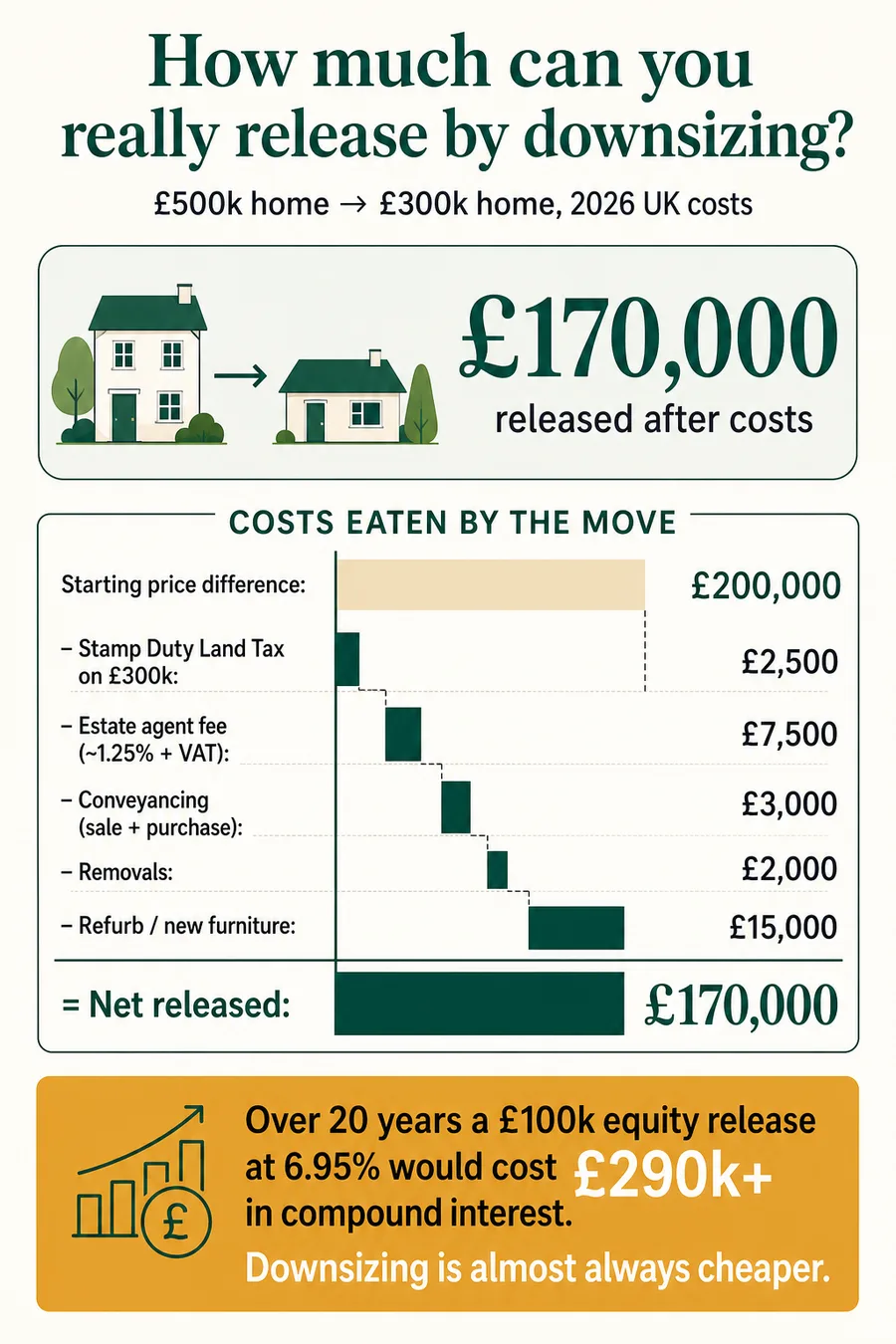

The real cost of moving in 2026/27

The headline price gap is the wrong number to plan around. Every move has six lines of cost, and on a £500k → £300k move they typically total £20,000-£30,000. The table below uses the same example as the calculator: a £500,000 sale and a £300,000 purchase in England, with a standard high-street estate agent at 1.25% commission and an average conveyancer.

| Cost line | Typical range | Worked example | Notes |

|---|---|---|---|

| Estate agent commission (inc. VAT) | 1.0%-1.5% + 20% VAT | £7,500 | On £500k sale at 1.25% + VAT. Fixed-fee online agents cheaper (~£1,000) but typically less service. |

| Stamp duty on new home | £0-£12,500+ | £5,000 | England/NI 2026/27 rates. Wales (LTT) and Scotland (LBTT) differ. No surcharge for main-home replacement. |

| Legal fees - sale + purchase | £1,500-£3,000 | £2,250 | Includes searches, Land Registry, disbursements. Leasehold transactions cost more. |

| Removals and packing | £1,000-£3,000 | £2,000 | Distance, volume and packing service drive cost. £600+ for a basic local job. |

| Refurb to sell + new place fit-out | £1,000-£10,000+ | £3,000 | Tidy-up paint, carpets, curtains, occasional new appliance. Excludes major works. |

| EPC, surveys, mortgage exit fee (if any) | £100-£1,000 | £250 | EPC is mandatory for the sale. Mortgage exit fees only apply if you have a remaining loan. |

| Total moving costs | £17,500 | ~3.5% of £500k sale value | |

| Net cash released (£500k − £300k − £17,500) | £182,500 | Tax-free under Private Residence Relief |

The single biggest swing factor is stamp duty. Buying a £300k bungalow costs £2,500 in SDLT. Buying a £400k purchase costs £7,500. A £500k purchase costs £12,500. A £700k purchase costs £22,500. Each step into the 5% band makes a meaningful dent in net release - which is why "trading sideways" (selling a £600k home, buying a £550k flat) rarely makes financial sense once stamp duty is in.

Stamp Duty Land Tax 2026/27 - the rates that bite

From 1 April 2025, the temporary SDLT thresholds were withdrawn and the residential rates returned to the bands set out below. These are the rates that apply throughout the 2026/27 tax year in England and Northern Ireland on a main residence - i.e. the home you are buying to live in, replacing your current main home, which is what downsizers do.

| Price band | SDLT rate | SDLT at top of band |

|---|---|---|

| Up to £125,000 | 0% | £0 |

| £125,001 to £250,000 | 2% | £2,500 |

| £250,001 to £925,000 | 5% | £36,250 |

| £925,001 to £1.5m | 10% | £93,750 |

| Over £1.5m | 12% | - |

Downsizing calculator: what you'd actually release

What an estate agent would list it at today.

Bungalow, flat or retirement apartment.

After a total of £19,750 in moving costs, you would net £180,250 of tax-free cash from this downsize.

That's roughly 4% of the sale value lost to friction. As a rule of thumb, anything below 4% is a tidy move; above 7% and you should look hard at whether the move is worth it for pure cash release.

Approximate. Uses 2026/27 SDLT rates for England and Northern Ireland on a main-home replacement. Wales and Scotland have different bands. Does not include Capital Gains Tax (a main home is normally exempt under Private Residence Relief), ground rent / service charges on a leasehold purchase, or event fees on retirement-village leases. Always confirm with GOV.UK and your solicitor before exchange.

Downsizing vs equity release - the 20-year cost

The financial case for downsizing rests almost entirely on this comparison. Equity release (specifically a lifetime mortgage) lets you borrow against your home without making repayments - but interest rolls up and compounds. Downsizing has high one-off costs but no interest. Over a typical 20-year retirement horizon, the gap is huge.

| Downsize to release £100k | £100k lifetime mortgage at 6% | |

|---|---|---|

| One-off cost | £15,000-£25,000 | £1,500-£3,000 advice + setup |

| Ongoing interest | £0 | ~6% compound (current ERC member avg.) |

| Debt after 10 years | £0 - done | ~£179,000 |

| Debt after 20 years | £0 | ~£320,714 |

| Inheritance impact | Smaller home in estate; released cash either spent, gifted or sits in estate | Debt is repaid from the home on sale; much less left for beneficiaries |

| Flexibility | Done once; you live in the new home | Stay in your home; can draw further (drawdown plan) |

| Means-tested benefits hit | Released cash above £6,000 starts to affect Pension Credit / Council Tax Support | Same - cash in the bank counts as capital |

Three real scenarios

Situation: Lives alone in the £550,000 four-bedroom house she and her late husband bought in 1996. Heating and council tax are eating her income; the garden is overwhelming; the spare bedrooms are empty.

Margaret sells for £540,000 and buys a £290,000 two-bedroom bungalow on a quieter road in the same town - five minutes from her daughter. Her costs:

- Estate agent fee (1.0% + VAT): £6,480

- SDLT on £290k: £4,500

- Legal fees (sale + purchase): £2,200

- Removals + 2 weeks of overlap: £2,500

- New carpets, paint, blinds at the bungalow: £4,500

- Total moving costs: ~£20,180

- Net released: ~£229,820 tax-free under PRR

She drops £20,000 into a Cash ISA emergency buffer, gifts £50,000 to her two grandchildren (starting the 7-year IHT clock), and invests the remaining £160,000 across a Stocks & Shares ISA and a low-cost multi-asset GIA to draw a £6,000/yr supplemental income. Her ongoing running costs at the bungalow are roughly £3,000/yr lower than the old house: warmer, cheaper to heat, smaller council tax band. Quiet, unspectacular, and a much better fit for the next twenty years.

Situation: London suburb, £820,000 home. Their only child and two grandchildren are in Sheffield. They want to be on the same school run as the grandkids.

The headline maths flatters them. A £820k London house traded for a £420k Sheffield bungalow gives £400k of gross equity. But London estate agent fees are higher (1.5% + VAT), the bigger purchase price puts them in the 5% SDLT band, and removals 180 miles north add up:

- Estate agent fee (1.5% + VAT): £14,760

- SDLT on £420k: £11,000

- Legal fees: £2,800 (includes leasehold review on flats they viewed)

- Removals 180 miles + packing service: £3,800

- New furniture, smaller windows, refurb on Sheffield property: £8,000

- Total moving costs: ~£40,360

- Net released: ~£359,640 tax-free

Even with high costs, they release nearly £360k - and, critically, they pick up the grandchildren from school three days a week. The financial release was the bonus, not the point. They use £200k to clear the small mortgage on their daughter's house (a legitimate lifetime gift, IHT clock starts at year 0), £30k for a £6k/yr drawdown holiday fund, and invest the rest. Carol describes it as "the best money decision we ever made, but only because it wasn't really about the money".

Situation: Owns his £450,000 three-bed home outright. Lived there for 41 years. Stairs now a serious daily challenge. Doesn't want to move and doesn't have family nearby.

For Brian, the right answer probably isn't downsizing at all. The cost-benefit:

- Option A - Downsize to a £280,000 ground-floor flat in the same town: net release after costs ~£155,000. But loses 41 years of memories, neighbours and familiarity. Statistically, retirees who move late after long tenure are at significantly higher risk of depression, falls and cognitive decline in the first 12 months.

- Option B - Adapt the existing home: stairlift (£3,500), walk-in shower downstairs (£6,000), downstairs bedroom conversion (£8,000), grab rails and lighting (£500). Total ~£18,000 - possibly with disabled facilities grant help from the council. He stays in his home, on his street, with the people he knows.

- Option C - Equity release £50,000 from his £450k home to fund adaptations, in-home care and a buffer. Costly over 20 years at 6% - but Brian is 78, and life expectancy at 78 is roughly 10-12 years. A £50k lifetime mortgage rolled up at 6% for 10 years is ~£89,500 of debt, leaving roughly £360,500 of his £450k home for the estate. Defensible if it means he keeps his independence and his home.

Brian goes with Option B plus a small equity release later if needed. The cheapest answer is not always the right answer - and the right answer is often "don't move". Read Age UK's housing options guide before making this call.

Best places to downsize in the UK

"Best" depends entirely on what you want. Below are five common downsizer profiles and where the maths and lifestyle tend to align. All locations cited are mainland UK; the Land Registry House Price Index (March 2026) is the source for the relative pricing.

| If you want… | Look at | Why it works |

|---|---|---|

| Maximum cash release | Coastal Lincolnshire (Skegness, Mablethorpe), East Yorkshire (Bridlington), parts of Cornwall away from the second-home belt | Bungalow stock is large and prices well below the South-East. £200k buys a real bungalow. |

| Walkable amenities, no car needed | Smaller cathedral cities - Salisbury, Winchester, Chichester, Truro, Lincoln, Durham | Compact centres, decent NHS access, train links, plenty of cafés and culture. |

| Stay close to grown-up kids in the SE | Hertford, Sevenoaks, Tunbridge Wells, St Albans, Reigate | Premium pricing; modest cash release. Worth it for time with family. |

| Built-in community, low-maintenance | Retirement villages (McCarthy Stone, Audley, Inspired Villages, ExtraCare Charitable Trust) | Single-storey or lift-served, on-site facilities. Check service charges and event fees first. |

| Low cost of living, milder climate | South Devon (Torbay, Newton Abbot), South Wales (Vale of Glamorgan), Pembrokeshire | Pleasant climate, established retirement communities, NHS access reasonable. |

Three universal checks regardless of postcode: distance to your GP and nearest A&E (ideally under 20 minutes by car or ambulance), supermarket within 1 mile, and a bus or train link that still works after you stop driving. Age UK's moving home guide covers the practical pre-move checks in detail.

Retirement villages - read the lease in full

- Annual service charge - current level (£2,000-£8,000+ a year typical) and the contractual mechanism for annual increases (RPI? CPI+? Uncapped?).

- Ground rent - peppercorn (£0), nominal (£1-£10/year) or substantial? Some older leases have rising ground rents; modern Leasehold Reform Act rules cap these on new leases.

- Event fees / exit fees / contingency fund contributions - the percentage of the eventual resale price taken by the operator. Industry ranges from 1% to 30%. This is the line that catches the most families on death of the leaseholder.

- Re-sale restrictions - does the operator have first refusal? An exclusive marketing period? What happens if the flat doesn't sell within X months?

- Care and support charges - are care services bundled in, optional or excluded? What happens if you need significant care later - can you stay or do you have to move out?

Use a solicitor experienced in retirement leasehold (not just general residential conveyancing). The Law Society maintains a Conveyancing Quality Scheme accreditation; ask specifically about retirement housing experience. ARCO (the Associated Retirement Community Operators) publishes a Consumer Code that members have signed up to - its presence is a useful baseline.

Tax: PRR, capital gains and inheritance

For most downsizers the tax position is delightfully simple. MoneyHelper's guidance highlights that downsizing is usually more cost-effective than equity release over the long term because there is no interest to pay. The bad news first: stamp duty. The good news: almost everything else is free of tax.

- Capital gains tax (CGT): none. Private Residence Relief (PRR) exempts the gain on your main home from CGT for every month you lived there as your only or main residence, plus the final 9 months of ownership automatically. A home you've lived in continuously is fully exempt.

- Income tax on released cash: none. The proceeds of selling your home are capital, not income. They are not taxed.

- Inheritance tax: here it gets interesting. Once cash is released from a home into your estate, it sits inside the inheritance tax net. If your estate (home + cash + pensions + investments) is above £325,000 nil-rate band, the excess is potentially taxed at 40% on death. The Residence Nil-Rate Band (RNRB) adds up to £175,000 of home value, passed to direct descendants. Downsizing doesn't usually lose you the RNRB - there are specific "downsizing addition" rules - but turning house into cash does remove a layer of natural IHT protection because cash is fully exposed.

Practical checklist before you exchange

Once you've decided downsizing is the right move, the difference between a smooth experience and a stressful one is usually preparation. Six things to do in the weeks before you list:

- Get three valuations and pick the middle agent, not the highest. The high-valuation agent often slashes the price weeks later. Negotiate the commission rate (1.0-1.25% + VAT is achievable on a £500k+ instruction).

- Declutter ruthlessly before listing. Buyers walk through bigger-feeling rooms. Hire a £200 skip. The new place will likely have less storage than you think.

- Commission an EPC and order a basic pre-sale check. EPC is legally required to market. Knowing the condition of your boiler and roof before a survey lands avoids late price renegotiations.

- Have your new-home shortlist ready before you accept an offer. Chain risk is the most common reason sales fall through. Knowing where you'd go (and ideally being able to move quickly) makes you a stronger buyer in your onward purchase.

- Brief your solicitor on the Replacement of Main Residence rules. If completion dates don't sync, you may have to pay the 5% second-home surcharge upfront - get the solicitor to ring-fence the funds and pre-warn HMRC.

- Plan what you'll do with the released cash before it lands. Cash sitting in a low-interest current account loses real value to inflation. Decide in advance: ISA allowances, GIA, gifts (with the 7-year IHT clock in mind), debt clearance, holiday fund.

Related guides

Frequently asked questions

- Should I downsize my home in retirement?

- Downsize if the gap between sale price and purchase price (minus moving costs) gives you a meaningful capital release, and if a smaller, more manageable home would genuinely suit how you want to live for the next 15-20 years. As a rough rule, you need at least £150,000-£200,000 of price gap before the maths comfortably beats staying put and using other options such as equity release or a retirement-interest-only mortgage. Moving costs (SDLT, agent fees, legal, removals, refurb) typically eat £15,000-£40,000, so a small downsize can release surprisingly little. MoneyHelper and Age UK both recommend treating downsizing as the default first option before any later-life borrowing.

- How much can I save by downsizing?

- On a typical £500,000 home to a £300,000 flat or bungalow move in England, the gross equity gap is £200,000 but after estate agent fees (~£7,500 inc VAT at 1.25%), stamp duty (£2,500 on a £300k purchase in 2026/27), legal fees (£2,000-£3,000 across sale and purchase) and £3,000-£5,000 for removals and small refurb, you typically net around £180,000-£185,000. Larger gaps release more in absolute terms, but stamp duty bites harder above £250,000 (5% band) and £925,000 (10% band). Our calculator further down the page gives you a personalised figure.

- Downsizing vs equity release: which is better?

- For most retirees who can physically move, downsizing is cheaper. A £100,000 lifetime mortgage at a fixed 6% interest rate, with interest rolling up, becomes a debt of roughly £320,000 after 20 years - versus a one-off moving cost of £20,000-£40,000 to release the same £100,000 by trading down. Equity release only wins where you genuinely cannot or do not want to move (a much-loved home near family and clinicians, no smaller property in the area at the right price, or physical mobility issues that make a move risky). MoneyHelper, the Equity Release Council and the FCA all expect advisers to discuss downsizing before recommending equity release.

- How much stamp duty will I pay if I downsize?

- On the new (smaller) purchase you pay full residential SDLT. From 1 April 2025 the 2026/27 rates in England and Northern Ireland are: 0% on the first £125,000; 2% on £125,001-£250,000; 5% on £250,001-£925,000; 10% on £925,001-£1.5m; and 12% above £1.5m. A £300k bungalow costs £2,500 in SDLT. A £400k purchase costs £7,500. A £500k purchase costs £12,500. Wales (LTT) and Scotland (LBTT) use different bands - check Welsh Revenue or Revenue Scotland. Downsizers don't pay the 5% second-home surcharge because the new home is replacing the main residence.

- Will I pay capital gains tax when I sell my home to downsize?

- No, in almost all cases. Private Residence Relief (PRR) means there is no Capital Gains Tax on the sale of your only or main home, however much it has gone up in value. PRR applies for every month you lived there as your main residence, plus the final 9 months of ownership automatically. You only get a CGT bill if part of the home was used exclusively for business, if you let part of it out beyond normal lodger arrangements, or if you owned a second home and need to nominate which is your main residence. HMRC publishes the full PRR rules in helpsheet HS283.

- What are the best places to downsize in the UK?

- There is no single "best" - it depends on your priorities. For lower prices and large stock of bungalows: coastal Lincolnshire, the East Riding of Yorkshire, parts of Wales, North Devon and rural Norfolk. For NHS access and family proximity in southern England: market towns just outside London commuter belts (Hertford, Sevenoaks, Tunbridge Wells, St Albans - premium pricing) or smaller cities (Salisbury, Winchester, Chichester). For purpose-built retirement villages: McCarthy Stone, Audley and Inspired Villages have schemes across England. Stay within practical reach of a hospital, your GP's catchment, and at least one close family member. Age UK's "downsizing" guide stresses checking the transport links, supermarket access and walking distance to amenities - these matter more than postcode when you no longer drive.

- What are the hidden costs of downsizing?

- Beyond the headline SDLT, agent and legal fees, the costs that surprise people are: refurbishment to make the old home sell (£2,000-£10,000 for new carpets, paint, kitchen tidy-ups); skip hire and decades of decluttering (£200-£1,000); new furniture and curtains for the smaller place (£2,000-£8,000); EPC and energy improvements if buyers expect them; ground rent and service charges on a flat or retirement village (£2,000-£6,000+ per year); event fees in some retirement villages (1-30% of resale price taken by the operator when you eventually sell); and the emotional cost of sorting through a family home. Build a £5,000-£10,000 contingency into your figures.

- Are retirement villages a good way to downsize?

- They suit some, not all. Pros: purpose-built for later life (level thresholds, wider doors, walk-in showers), built-in community, on-site activities, often a warden or care available, and freedom from house and garden maintenance. Cons: service charges typically £4,000-£8,000 a year and rising with inflation; significant event fees / exit fees on resale at some operators (sometimes 10-30% of the eventual sale price); ground rent on leasehold schemes; and resale can be slower than mainstream housing. Read the lease in full, get a solicitor experienced in retirement leasehold to review event fees, and price-compare against a freehold bungalow in the same town.

- Does downsizing affect inheritance tax?

- It can - usually positively, sometimes negatively. The Residence Nil-Rate Band (RNRB) currently lets you pass up to £175,000 of home value to direct descendants free of IHT, on top of the £325,000 nil-rate band. If you downsize, the "downsizing addition" rules let your estate still claim the full RNRB you would have qualified for before the move, provided you still leave assets of equal value to direct descendants. So you usually do not lose RNRB just by trading down. But the released cash now sits in your estate, where it can attract IHT at 40% above the nil-rate bands - unless you spend it, gift it under the 7-year rule, or move it into IHT-efficient wrappers. Take advice if your estate is near the IHT thresholds.

- Is it worth downsizing for £100,000?

- Often not, once costs are taken into account. A £400k → £300k move in 2026/27 releases £100,000 of gross equity but spends roughly £15,000-£20,000 on moving costs (agent ~£6,000 inc VAT, SDLT £2,500, legal £2,000, removals £1,500, refurb £3,000), netting around £80,000-£85,000. You also lose any future house-price growth on the £100k you no longer have invested in property. The move makes more sense if the smaller home suits your future health needs, releases ongoing maintenance and energy costs, or moves you closer to family. If pure cash release is the only goal, a £100k gap may not be enough - consider whether £150k+ gives you a better margin of safety.